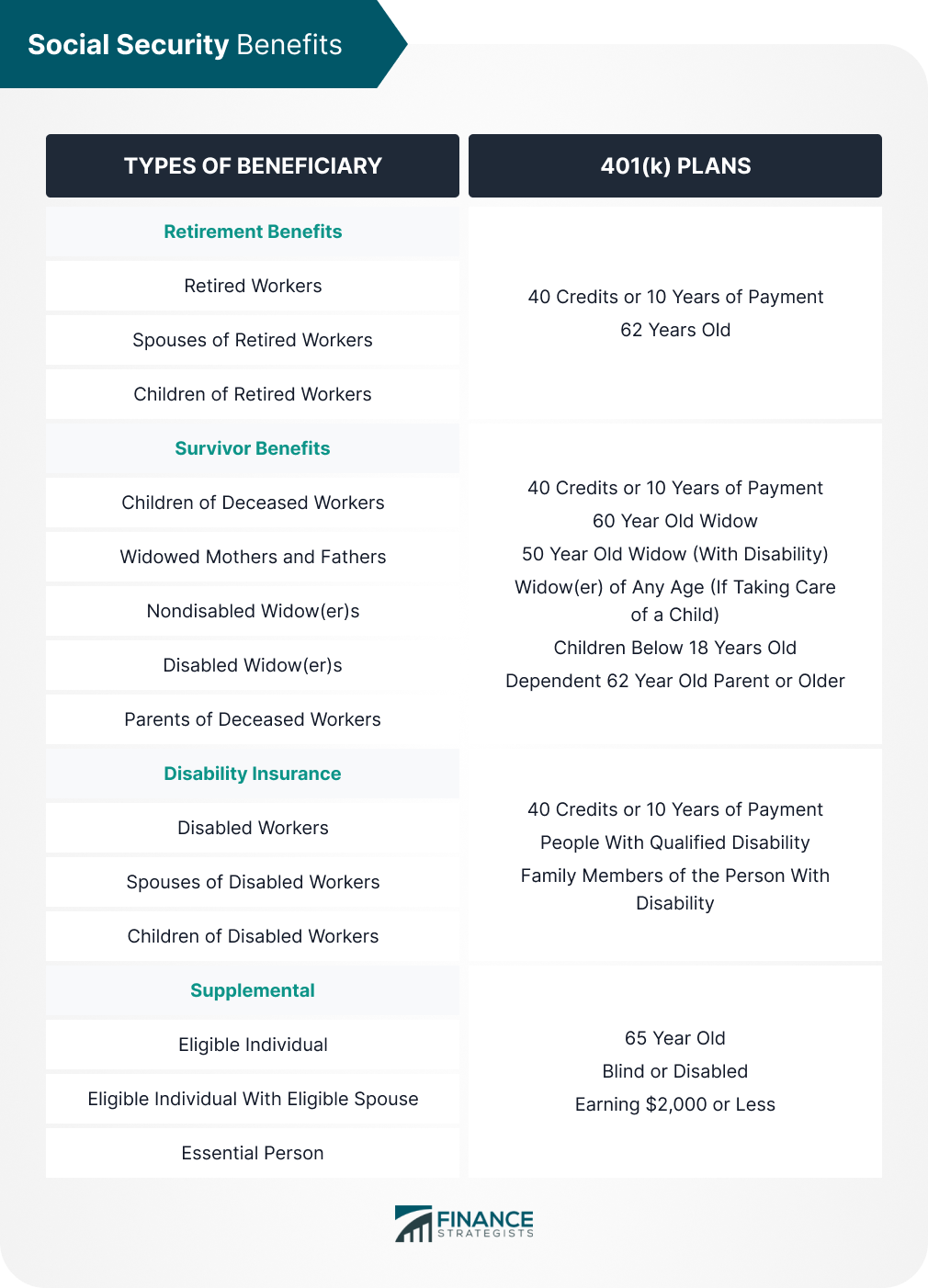

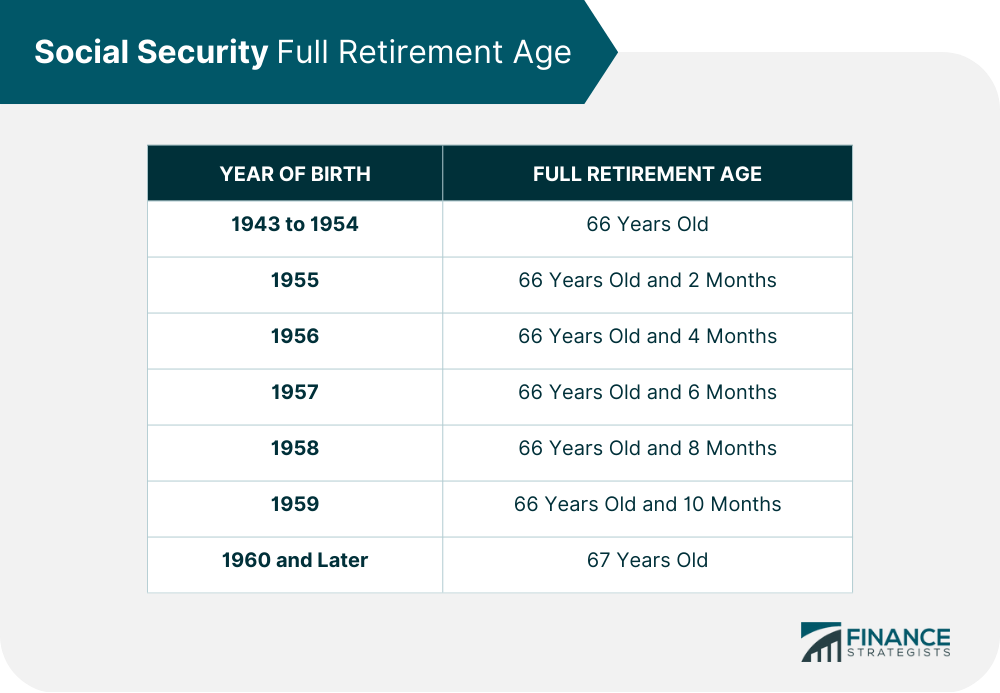

Social Security is a government-operated social insurance program that provides financial assistance to retirees, disabled workers, and their families. It also helps eligible survivors of deceased workers and other particular beneficiaries. The official name of Social Security is the Old-Age, Survivors, and Disability Insurance (OASDI) program. It is governed by the Social Security Administration (SSA), which collects payroll taxes from employers and employees to fund the program. Social Security is the primary source of income for many retired Americans. In fact, the total number of Social Security beneficiaries is estimated to be at around 68 million. The Social Security Act was signed into law in 1935 by President Franklin D. Roosevelt as part of the New Deal. After World War I, American society was primarily urban and industrialized. Americans, more than ever, relied on cash wages, and most consumed their entire savings. Much older and nearing old age people were living in poverty. There was a need to establish a federal social insurance system to ensure income security for the elderly. The 1939 amendment also included benefits for surviving spouses and dependents of deceased workers. The 1954 amendment added disability benefits, and the 1956 amendments extended coverage to various types of workers. The Social Security Act has been amended several times to reflect changes in the labor force, social needs, and economic conditions. It is one of the world's most extensive government programs, disbursing hundreds of billions of dollars annually. Social Security works by collecting compulsory worker contributions into a huge pot and paying out benefits to eligible individuals. You must have a Social Security number to work and pay taxes. The SSA uses this number to track your earnings while working and your benefits at the time you apply for benefits. Benefits are classified into four categories based on who receives them. There are four benefits: The maximum Social Security benefit you will receive is determined based on your lifetime earnings, a formula set by the SSA, and the age you choose to start receiving benefits. Supplemental Security Income (SSI) benefits are also available to certain people with limited income and resources who are disabled, blind, or age 65 or older. To qualify for the program, individuals must meet specific requirements. In general, applicants must have obtained a minimum number of work credits based on their earnings and tax payments and reach a particular age qualification. To become entitled to Social Security retirement benefits, you must have earned at least 40 credits via employment and payment of Social Security taxes. This requirement equates to at least ten years of work; benefits can be taken as early as age 62. Beneficiaries of survivor benefits must satisfy criteria such as widows must be 60 years or older and 50 years or older if the widow has a qualifying disability. They can be any age if they care for a child with a disability or a child under 16. Children can also receive survivor benefits if they are under 18 years old or if they have a disability. Benefits may also be available to 62-year-old parents and older who relied on a departed worker for at least half their income. Disability benefits are available for people who cannot work due to a long-term physical or mental condition that will last for more than a year and is severe enough to affect their ability to work and live independently. Their family members are also eligible for the benefit. People at least 65 years old, blind, or disabled with limited income and resources may also receive Supplemental Security Income benefits. The amount of these benefits varies by state. Individuals who have resources of $2,000 or less are eligible. The work credits requirement varies with the age of disability. The full retirement age (FRA) is when individuals can begin collecting Social Security retirement benefits without penalty. The FRA ranging from 66 to 67 years old varies with birth year. Retirement eligibility starts at 66 years old for those born from 1943 to 1954. The retirement age increases by a few months for each birth year until it reaches 67 for individuals born in 1960 or later. Your benefit amount will increase if you wait until 70 years old before claiming your benefits. Social Security taxes are the lifeblood of the Social Security program. Social Security is a government-operated social insurance program that provides financial assistance to retirees, disabled workers, and their families. It also helps eligible survivors of deceased workers. Social Security is one of the primary sources of income for retirees. In 1935, the Social Security Act became law and created the retirement program to ensure Americans would have a secure and stable income after retiring from the workforce. It has been amended and modified to reflect economic and social changes. The program works by taking taxes from current workers and investing them in providing benefits for those currently receiving Social Security. The amount of money taken in taxes depends on how much an individual earns. Social Security can come from retirement, disability, and survivor benefits. Eligibility requirements vary for each type of benefit. Generally, they include 40 credits or 10 years of work history, the minimum age for survivors, and proof of a qualifying disability. Taxes associated with Social Security are based on wages earned up to the cap limit, adjusted annually. These taxes are the sources of funding for the Social Security program. They typically are shouldered equally by both employers and employees. What Is Social Security?

History of Social Security

How Social Security Works

That means you need $7,560 in earnings to earn the maximum four credits in 2026. The amount required to earn one credit generally increases each year as average wages rise.

For comparison, in 2025, you earned one credit for every $1,810 in earnings, up to the same four-credit annual maximum.

The taxable maximum for Social Security will increase in 2026 to $184,500, up from $176,100 in 2025. This is the maximum amount of earnings subject to Social Security payroll tax for the year.

The Social Security tax rate remains unchanged in 2026 at 6.2% for employees and 6.2% for employers. Self-employed individuals generally pay both portions, for a combined 12.4% Social Security tax rate.

The money is deposited into two Social Security trust funds: the Old-Age and Survivors Insurance Trust Fund, which pays retirement and survivor benefits, and the Disability Insurance Trust Fund, which pays disability benefits.Types of Social Security Benefits

Retirement Benefits

The SSA then calculates your average indexed monthly earnings based on your highest 35 years of earnings. That figure is used to determine your primary insurance amount, which is the basis for your retirement benefit.

Your claiming age also affects your monthly payments.

Claiming benefits before full retirement age generally reduces your monthly benefit, while delaying benefits can increase your monthly payments.

In 2026, the maximum Social Security benefit for a worker retiring at full retirement age is $4,152 per month, up from $4,018 per month in 2025.

For 2026, the Social Security cost-of-living adjustment, or COLA, is 2.8%, compared with 2.5% in 2025 and 3.2% in 2024.

Social Security benefits increase by 2.8% beginning with December 2025 benefits, which are payable in January 2026.

Based on SSA estimates, the average monthly benefit for a retired worker is expected to increase from $2,015 before the 2026 COLA to $2,072 after the 2026 COLA, an increase of about $57 per month.

The SSA also provides separate average benefit estimates for spouses of retired workers, aged widow(er)s, disabled widow(er)s, and disabled workers.Survivor Benefits

Survivor benefits are paid to eligible family members of a deceased worker who paid into Social Security and earned enough credits to qualify.

These benefits may be available to a surviving spouse, divorced surviving spouse, dependent children, and, in some cases, dependent parents.

In many cases, eligible survivors may receive 75% to 100% of the deceased worker’s benefit amount, depending on the survivor’s age, relationship to the worker, disability status, and whether the survivor is caring for the worker’s child.

Children may generally receive up to 75% of the deceased worker’s basic benefit, while a widow or widower at full retirement age or older may receive up to 100%.

For 2026, the Social Security cost-of-living adjustment, or COLA, is 2.8%. According to SSA estimates, the average monthly benefit for an aged widow(er) alone will increase from $1,867 before the 2026 COLA to $1,919 after the 2026 COLA.

For a widowed mother with two children, the average monthly benefit will increase from $3,792 to $3,898.

The SSA’s April 2026 Monthly Statistical Snapshot shows that survivor benefits averaged $1,625.56 per month across all survivor beneficiaries.

The same table provides separate averages for children of deceased workers, widowed mothers and fathers, nondisabled widow(er)s, disabled widow(er)s, and parents of deceased workers.Disability Benefits

Disability benefits are paid to eligible workers who have a qualifying long-term disability and enough Social Security work credits.

These benefits may also be paid to eligible family members, including spouses and children of disabled workers.

For 2026, the Social Security COLA is 2.8%. The average monthly benefit for disabled workers increased to about $1,630, while a disabled worker with a spouse and children receives about $2,937 on average.Supplemental Benefits

For 2026, the maximum federal SSI payment is $994 per month for an individual, $1,491 for an eligible couple, and $498 for an essential person. As of April 2026, the average SSI payment was $738.22 per month.

Social Security Eligibility

Retirement Benefits

Survivor Benefits

Disability Benefits

Supplemental Benefits

Social Security Full Retirement Age

Social Security Taxes

Self-employed individuals generally pay both shares, for a total of 12.4%.

A wage cap is adjusted annually, and wages above this amount are not subject to Social Security tax.

The Social Security wage cap is $168,600 in 2024, $176,100 in 2025, and $184,500 in 2026.

For an individual earning $190,000 in wages:

2024 Social Security Tax Due: 6.2% of $168,600 = $10,453.20

2025 Social Security Tax Due: 6.2% of $176,100 = $10,918.20

2026 Social Security Tax Due: 6.2% of $184,500 = $11,439.00Final Thoughts

Social Security FAQs

The process is simple if you need a new Social Security card. First, fill out an application for a Social Security Card (Form SS-5). You can find this form online at the official Social Security website or pick one up at any local Social Security office. Next, provide proof of your identity and either citizenship or lawful non-citizen status. Finally, submit your completed application and proof of identity to a local Social Security office.

Starting in 1983, Social Security benefits are taxable beyond certain income thresholds. No taxpayer, regardless of income, has the whole amount of their Social Security benefits taxed. The highest category comprises 85% of the full benefit.

Applying for Social Security benefits can be done online at the official Social Security website or in person at any local Social Security office. To apply for benefits, you must provide proof of your identity and either citizenship or lawful non-citizen status. You may also need to provide marriage, military service, and work history documents. Lastly, you must fill out an application for Social Security benefits.

You can check the status of your Social Security benefits by visiting the official Social Security website and using their My Social Security feature. This tool allows you to review your payment history, make changes to personal information, and verify that all information is correct. Additionally, you may call or visit a local Social Security office for assistance with checking your status.

Social Security benefits are computed based on your lifetime earnings up to the Social Security taxable wage base. This amount changes from year to year and is adjusted for inflation. Your yearly earnings are indexed to account for wage growth over time. The Social Security Administration then calculates a benefit amount based on these indexed wages by applying a formula that considers work history and age.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.