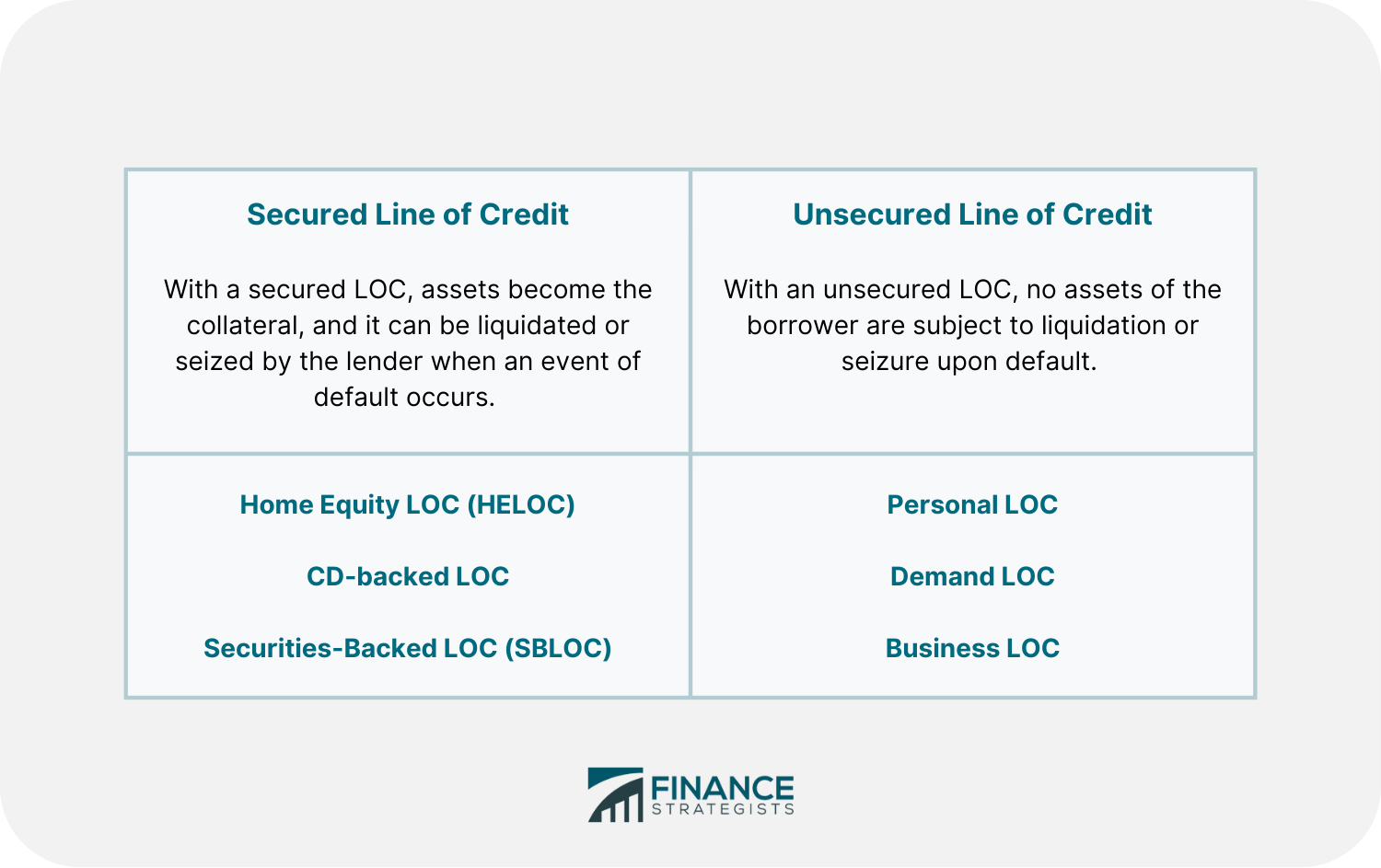

A line of credit is a predetermined amount of funds that a financial institution, such as a bank, makes available to an individual or a business which the borrower pays interest on. Depending on the type of LOC, the borrower either receives a lump sum or is allowed to withdraw from the line of credit at any time, up to the maximum amount or the credit limit approved. For some types of LOC, the credit limit will replenish as the borrowed money is repaid. This means that the borrower may continue borrowing again, as needed. Line of credit can come in several forms, including home equity line of credit (HELOC), personal line of credit, and small business credit line. To obtain a line of credit, borrowers must first apply for and be approved by a financial institution. Requirements for applying for lines of credit may vary by the type and lender. The approval process is usually heavily influenced by the borrower's credit rating. Thus, borrowers who have good or excellent credit have better chances of getting approved at the lowest interest rates available. Once approved, the lender sets interest, repayments, and other terms for the line of credit. Then, to provide access to the funds, some lines of credit may allow the borrower to write checks, while others include a type of credit card. Just like a traditional loan, a line of credit will charge interest on the money that is borrowed. However, the interest charged on the line of credit is based only on the actual amount withdrawn by the borrower and not on the entire amount available. A significant difference between a line of credit and a traditional loan is that the latter involves borrowing a sum of money and paying it on an installment basis within a given period. With a traditional loan, you cannot continually withdraw new money against the same loan. On the other hand, when you apply for a line of credit, you are applying for regular access to the approved funds when needed. For most lines of credit, you can take out money repeatedly as long as you are able to repay the amount you borrowed, since this replenishes the amount set in the credit limit. For instance, a borrower might need some extra money for home repairs. A traditional loan will give them $15,000 upfront, if they qualify. Once they receive the loan amount, they have to start repaying a portion of the principal amount with interest immediately, even if they have not used the funds yet. In contrast, if they get a line of credit for the same amount, they can borrow only what they need, when they need it. For example, in the first month, they might use only $3,000 for roof replacement and then $7,000 in the second month for kitchen renovations. With this set-up, they would only need to pay $10,000 plus interest instead of paying for the entire approved credit limit. There are several types of LOCs which can all be classified under two categories: secured or unsecured. With a secured LOC, the lender has established a lien against an asset that belongs to the borrower. The asset becomes the collateral, and it can be liquidated or seized by the lender in the event of a default. Because the lender has more certainty of getting the money back, a secured LOC typically comes with a significantly higher credit limit and lower interest rate than an unsecured LOC does. The common versions of secured LOC include: HELOCs are secured by your home’s equity, which is computed by subtracting your remaining mortgage from the market value of your home. Very few lenders will let you borrow the total amount of your home equity. Generally, they issue HELOCs equivalent to around 60% to 85% of the home’s equity. For instance, if your home is worth $350,000 and you owe $200,000 on your mortgage, then you have $150,000 in home equity. So, if you get approved for a HELOC worth 80% of your home’s equity, then you have a credit limit of around $120,000. HELOCs often have two important stages: the draw period and the repayment period. In the draw period, the borrower can get access to the available funds up to their credit limit. If the borrower repays the principal amount, the credit limit is replenished and the funds may be borrowed again. During the repayment period, the borrower must repay the outstanding balance of both the principal amount and the interest. On top of the balance, HELOCs also typically have closing costs, which can include the appraisal fee on the asset used as collateral. Using HELOCs has some drawbacks, such as the buyer losing their home or property should they default on their payments. However, it is good to note that the interest paid on a HELOC may be deductible if the money is used to "buy, build or substantially improve" the property in question. CD-backed LOC allows an individual to borrow money with a certificate of deposit (CD) as collateral. This option is more easily available to those with low credit scores or limited credit histories who may disqualify for certain types of loans. However, it also poses a risk. Borrowers may lose their CD if they fall behind on their payments. SBLOCs is a type of line of credit that uses the assets in the borrower’s investment portfolio as collateral. With this set-up, it is as if the borrowers can access 50% to 95% of the value of their assets without having to liquidate any of their securities. This type of LOC has a limitation, though. The borrower may not use the funds to buy or trade securities. SBLOCs also often carry risks, including potential tax consequences and the possibility of selling your holdings, which could affect your long-term investment goals. With an unsecured LOC, no assets of the borrower are subject to liquidation or seizure upon default. With no collateral, the lender expects a greater risk in approving an unsecured LOC. Therefore, to make up for this risk, interest rates are also generally higher and the borrowing limits are generally lower compared to secured loans. Credit cards are one of the most common examples of unsecured LOCs. When the cardholder defaults, there is nothing the issuer of the card can seize for payment. This is one of the reasons why the interest rates of credit cards are so high. Other types of unsecured LOCs are: A personal LOC is an unsecured, set amount of funds from which an individual can borrow, repay, and re-borrow for a given period of time. Similar to a credit card, PLOC can be a great option for emergency expenses or to help manage irregular cash flow. A business LOC is functionally the same as that of a personal LOC. However, it may have higher credit limits and are targeted specifically for businesses. Among other things, companies may use this line of credit to address short-term cash flow issues. Although functionally the same as the previously mentioned types of LOC, with the demand LOC, the lender can decide to recall the amount borrowed at any time. Then, depending on the agreed upon terms, the payback can be interest plus principal or interest only. Because of its unpredictable repayment schedule, this type of LOC might be rarely used. You can apply for either a secured or unsecured line of credit depending on your needs. Here is an overview of the different types of lines of credit: Aside from categorizing LOCs as secured or unsecured, they can also be divided into revolving and non-revolving. A revolving LOC can be used repeatedly up to its credit limit as long as the account is still open and payments are made on time. While in a non-revolving LOC, the funds available for credit do not replenish even after payments are made. The account is closed and cannot be used again once you pay the LOC in full. For both types, funds can be borrowed for various purposes. There is also an interest charge and an established credit limit. What differentiates these two types is whether repaying the principal amount replenishes the credit limit. If it does, the borrower may borrow from it again in a never-ending, revolving cycle. There are many advantages to using a line of credit. Here are some of them: Lines of credit offer flexibility in borrowing and repaying. You can use as much or as little funds from your line of credit as you need. Then, you can make payments in installments or in a lump sum, and the interest to be charged will be based on the amount of funds that you have used. With a line of credit, you can borrow funds easily and quickly without going through the formal loan process every single time. This is helpful in addressing short-term financial needs or emergency expenses. A line of credit can help you build up your credit history. As long as you make your payments on time, a line of credit will improve your credit score. There are also some disadvantages to using a line of credit. Some of them are: It can be tempting to overspend with a line of credit since it is easy to access funds. This can lead to debt problems and financial troubles if not handled properly. Unsecured LOC usually has higher interest rates compared to secured LOC. This is because there is a higher risk for the lender when a loan is not backed by collateral. Since repayment schedules are more flexible with LOCs, interest rates vary depending on the balance of the principal amount borrowed. Therefore, it might be difficult to predict how much total interest you will pay when you obtain a line of credit, as opposed to traditional loans which have fixed repayment schedules and interest rates. Lines of credit are usually not subject to the same regulatory protection as traditional loans. For example, there is no cap on the interest rates that lenders can charge and they are also not governed by the Truth in Lending Act (TILA). This means that lenders can change terms at any time without notice, which can be difficult for borrowers to keep up with. Among other things, this may result in drawbacks like higher interest rate and exorbitant late payment fees. Prospective borrowers should take note of specific requirements to qualify for a line of credit. As with any credit application, borrowers must provide the lender with documents that can establish a record of their earnings and a history of their timely payments. This can also include debt-to-income ratio, net worth, and cash on hand. These details allow lenders to assess the borrower’s financial condition and see if they can be relied upon to pay back the money owed. Lenders’ assessments are also influenced by the borrower’s credit score. A higher credit score means that the borrower is low-risk and is qualified for a line of credit with better terms. A line of credit is a flexible loan that can be used for various purposes. It offers easy access to funds and interest rates are variable compared to traditional loans. However, there are some disadvantages of using a line of credit, such as the temptation to overspend and higher interest rates on unsecured LOC. If you are considering getting a line of credit, make sure to assess your needs and compare offers from different lenders. This will help you find the best option that fits your financial situation.What Is a Line of Credit (LOC)?

How Does a Line of Credit Work?

Types of Line of Credit

Secured Line of Credit

Home Equity Line Of Credit (HELOC)

CD- Backed Line of Credit

Securities-Backed Line of Credit (SBLOC)

Unsecured Line of Credit

Personal Line of Credit

Business Line of Credit

Demand Line of Credit

Revolving vs. Non-Revolving Line of Credit

Advantages of Line of Credit

Disadvantages of Line of Credit

How to Get a Line of Credit

The Bottom Line

Line of Credit (LOC) FAQs

You can use a LOC for various purposes, such as funding a business, consolidating debt, or paying for home renovations.

A line of credit is a flexible loan from banks or financial institutions that involves a defined amount of funds that you can easily access as needed and repay either immediately or over time.

A line of credit can help you build up your credit. Therefore, as long as you pay on time, a line of credit will improve your credit score and history.

A traditional loan is the best option if you need to finance one-time expenses. However, if you are looking to fund ongoing expenses or you want to reserve money in emergency situations, then a line of credit is a better option.

Some of the risks of using a line of credit include overspending, higher interest rates on unsecured LOC, and the absence of regulatory protection.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.