A defined contribution plan is a tax-deferred retirement plan in which employees contribute a predetermined amount or a percentage of their paychecks to an account intended to fund their retirement. Employees can invest pre-tax dollars in the financial markets, which can grow tax-deferred until retirement under such plans. As an added benefit, the sponsoring company can match a portion of employee contributions. Companies and organizations commonly use defined contributions plans such as 401(k) and 403(b) to encourage employees to save for retirement. These plans impose restrictions on when and how each employee can withdraw funds from these accounts without penalties. Defined contribution plans differ from defined benefit plans because they offer no guarantees, and participation is voluntary and self-directed. The employee benefits upon retirement cannot be determined because contribution levels can change, and investment returns can fluctuate over time. Defined contributions plans invest pre-tax dollars in stock market indices that grow tax-deferred. This means that income tax will be paid on withdrawals at retirement age, with required minimum distributions (RMDs) beginning at age 73. If it is withdrawn before the age of 59 1/2, a 10% penalty will be imposed unless certain exceptions are met. Companies providing defined contribution plans must comply with laws regulated by the Employee Retirement Income Security Act (ERISA). Defined contribution plans such as 401(k)s offer several advantages that can make saving for retirement more accessible and more efficient. An essential advantage of defined contribution plans is their tax benefits. Contributions are taken from pre-tax earnings, allowing participants to report lower income for the applicable tax year. Additionally, any investment returns earned within the plan defer taxes until withdrawal, allowing participants to enjoy more time growing their money unaffected by taxation. Matching contributions may also be made to employer-sponsored defined contribution plans. Employers typically match contributions at a rate of $0.50 per dollar. Some companies may offer a dollar-for-dollar match, up to a certain percentage of an employee's salary, typically 4% to 6%. If your employer matches your contributions, it is ideal to contribute up to the maximum allowable amount. A set percentage of an individual's salary is automatically deducted every month and put into the plan. This gives retirees peace of mind that their savings will build slowly but surely in the background without extra effort. In 2026, contributions to an individual retirement account (IRA) are capped at $7,500 ($7,000 for 2025) per year or $8,600 ($8,000 for 2025) if you are 50 or older. On the other hand, employees can save up to $24,500 ($23,500 in 2025) in defined contribution plans such as a 401(k) or 403(b), plus an additional $8,000 ($7,500 in 2025) if they are 50 or older. Total employer and employee contributions are $72,000 ($70,000 for 2025), or $80,000 ($77,500 for 2025) if you are 50 or older. These numbers prove that contributing long term towards retirement can create an excellent opportunity for financial security. Defined contribution plans like 401(k)s or IRAs can carry significant disadvantages for individuals saving for retirement. One major disadvantage of defined contribution plans is that they do not guarantee a specific retirement income. Investment choices and decisions regarding contributions determine the success or failure of these types of accounts. Since defined contribution plan funds are typically invested in stocks and bonds, they are subject to market fluctuation. There is no guaranteed return on your investment. Additionally, any profits or losses you experience are yours alone, and you may end up with less than you expected. The investment selections that employers offer may be limited, preventing savers from customizing their portfolios and taking advantage of various market trends. Therefore, those unsatisfied with their defined contribution plan might supplement it with an IRA, which offers additional options and flexibility. Suppose your plan does have excessively high fees. In that case, maximizing employer-matching contributions, and then moving the rest of your retirement contributions into an IRA makes the most financial sense. This can reduce expenses, minimize taxes, and ensure better returns in the long run. With the prevalence of employer-sponsored defined contribution plans and 401(k) accounts, more people have easy access to retirement investments. However, some employers require employees to remain at the company for years before they gain full ownership of employer contributions. Employees must become informed about their primary plan's vesting rules. Defined contribution plans may require you to take RMDs at 73 years of age. These RMDs can significantly increase your taxable income regardless of whether you need the money or not. Reducing your RMDs by rolling them into a Roth IRA or purchasing a qualified longevity annuity contract (QLAC) may be possible. Both options can provide meaningful savings and financial security. There are many different types of defined contribution plans available, so it can be helpful to understand the benefits and drawbacks of each to make the best decision. Employees of public or private for-profit companies and businesses are entitled to 401(k) plans. Employees can use a qualified profit-sharing plan to set aside part of their income in individual accounts. At the same time, employers can make contributions to their employees' accounts. Elective salary deferrals reduce employees' taxable income except for designated Roth deferrals. A 403(b) plan, known as a tax-sheltered annuity (TSA) plan, is a type of retirement plan provided by public schools and specific charitable organizations. A 403(b) plan, like a 401(k), allows employees to defer a portion of their salary into individual accounts. The 457 plans are tax-advantaged retirement plans similar to 401(k)s offered by state and local governments and specific tax-exempt organizations. The TSP is a tax-deferred retirement and investment plan that provides federal employees the same savings and tax advantages that many private corporations offer to their employees through 401(k) plans. Companies with 100 or fewer employees can take advantage of Savings Incentive Match Plans for Employees (SIMPLE) IRAs. SIMPLE IRA contributions and earnings can be withdrawn at any time, subject to the same restrictions as traditional IRAs. A SEP IRA is a type of retirement plan that is available to small business owners and qualified employees. Contribution and income limits are relatively high. With defined contribution plans, the employee controls how much money to contribute and where that money is invested. It is up to them to actively manage their investments and ensure enough funds are available for retirement. On the contrary, in a defined benefit plan, the employer carries this responsibility and must provide fixed benefits at retirement without the option of selecting individual investments or alternative funds. Take a traditional pension plan as an example; employers contribute most of the funding on behalf of employees. This pension plan provides a guaranteed level of income during retirement, usually based either on a fixed amount or as a percentage of the average wages earned. Overall, a defined contribution plan offers no guarantee that you will receive any specific amount upon retirement. Your pension income relies solely on the contributions and performance of your investments. These plans carry risks and the potential for less retirement income than traditionally defined benefit plans. But you may find comfort in directly managing where and how much you choose to invest when setting up the plan. A defined contribution plan is a tax-deferred retirement plan in which employees contribute a set amount or a percentage of their income to a retirement account. Such investments grow tax-deferred, meaning no taxes are paid until the money is withdrawn. One key benefit of these plans is that they offer flexibility. Employees can choose how much they wish to contribute and which investments they want to make. However, their success also depends on market conditions and employee decisions; the return on the invested funds may be different than expected. A defined contribution plan only specifies how much each party - the employer and the employee - contributes to a retirement account. In contrast, a defined benefit plan determines how much retirement income employees will receive once they retire. Some examples of defined contribution plans are 401(k), 403(b), 457, TSP, SIMPLE IRA, and SEP IRA. Whether defined contribution plans are suitable for someone’s circumstances depends on their lifestyle, risk tolerance, and other retirement goals. Before committing to any long-term savings plan, seeking help from a retirement planning professional is recommended.What Is a Defined Contribution Plan?

How Defined Contribution Plans Work

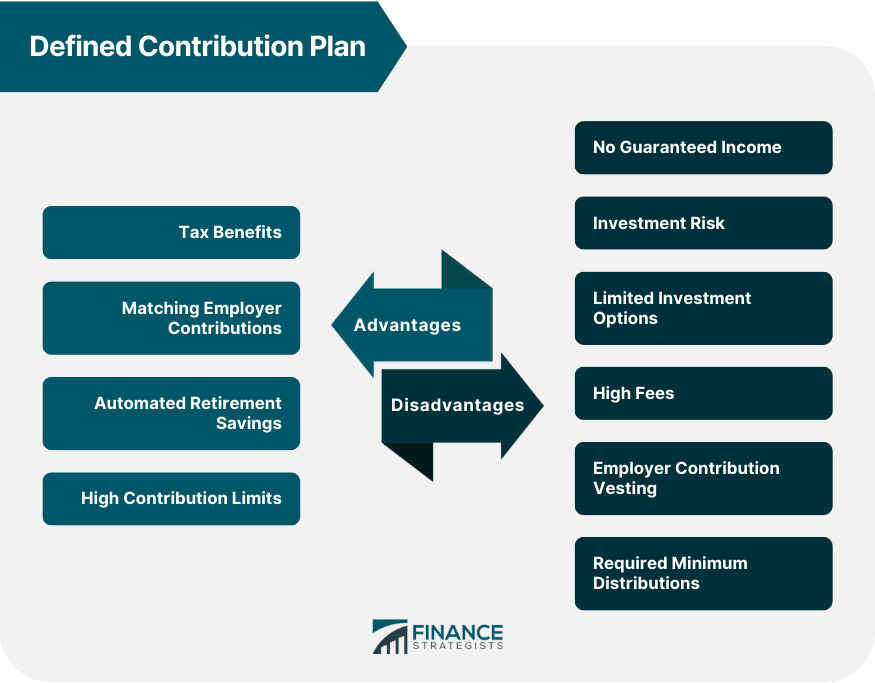

Advantages of a Defined Contribution Plan

Tax Benefits

Matching Employer Contributions

Automated Retirement Savings

High Contribution Limits

Disadvantages of Defined Contribution Plans

No Guaranteed Income

Investment Risk

Limited Investment Options

High Fees

Employer Contribution Vesting

Required Minimum Distributions

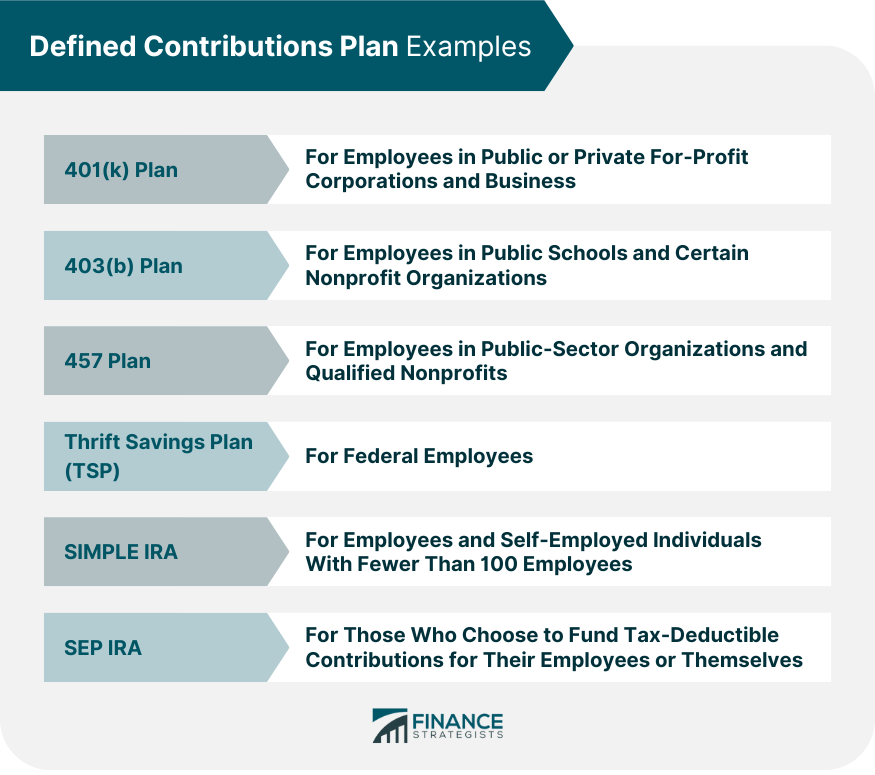

Examples of Defined Contribution Plans

401(k) Plan

403(b) Plan

457 Plan

Thrift Savings Plan (TSP)

SIMPLE IRA

SEP IRA

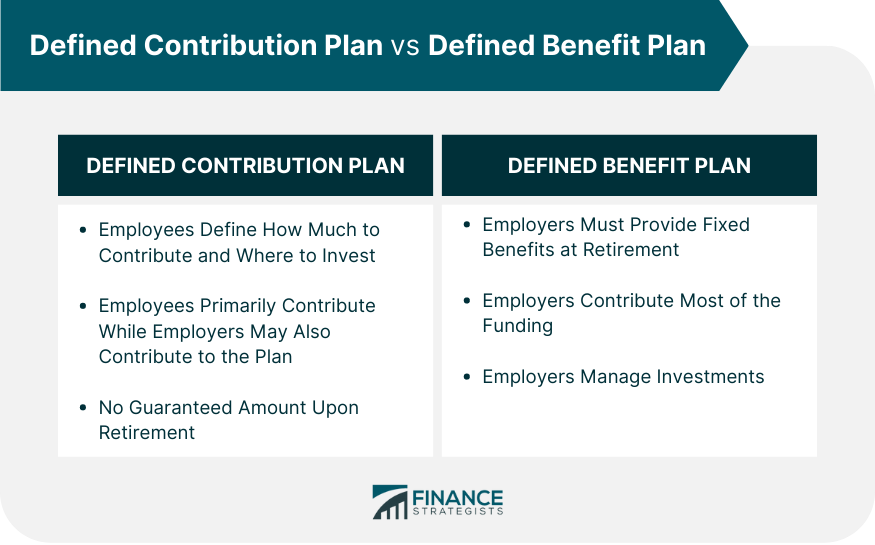

Defined Contribution Plan vs Defined Benefit Plan

Final Thoughts

Defined Contribution Plan FAQs

Defined contribution plans such as 401(k) or 403(b) allow employees to save up to $24,500 in 2026 ($23,500 in 2025), and those 50 years or older can save an extra $8,000 ($7,500 in 2025). Total employer and employee contributions are $72,000, or $80,00 if you are 50 or older. Whereas, contributions to an individual retirement account (IRA) are capped at $7,500 per year or $8,600 if you are 50 or older.

You can cash out your defined contribution pension plan with certain restrictions. Generally, you can withdraw all or some of your balance after reaching age 59 1/2. Before then, you may incur a 10% early withdrawal penalty and regular income taxes on the amount withdrawn.

A defined contribution plan is an employer-sponsored retirement savings account where employees contribute a set amount each period and receive benefits based on their investment earnings and employer contributions. A defined benefit plan is an employer-sponsored pension account where employers guarantee specific benefits at retirement depending on factors like salary history and years of service.

Examples of defined contribution plans include 401(k)s, 403(b)s, 457s, IRAs, and profit-sharing plans. Each plan has different features to meet the individual needs of employers and employees.

The main benefits of a defined contribution plan include tax savings on contributions and earnings, flexibility in investment choices, potential employer matching funds, and portability if you change jobs. Additionally, many defined contribution plans offer asset protection from creditors in certain situations. Defined contribution plans can effectively save for retirement while enjoying the numerous associated tax advantages.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.