Health insurance plays a crucial role in ensuring access to healthcare and providing financial protection for individuals and families. This article will explore the various aspects of health insurance, including its types, components, and impact on healthcare. Health insurance is a contract between an insurer and an individual or group, where the insurer agrees to pay for a portion of the insured's medical expenses in exchange for a premium. The purpose of health insurance is to help individuals manage the financial risk associated with illness or injury, and ensure access to necessary healthcare services. There are various types of health insurance plans, designed to meet the diverse needs of individuals and families. These plans can be categorized as private, public, or international health insurance, each with its unique features and benefits. Having health insurance is essential for maintaining good health, as it provides access to preventive care and early detection of diseases. It also offers financial protection against high medical expenses, helping individuals avoid medical debt and bankruptcy. Individuals have different options for obtaining health insurance coverage, depending on their eligibility, needs, and preferences. These options include private and public health insurance, as well as international health insurance for those traveling or living abroad. Private health insurance is offered by private companies and can be obtained through employer-sponsored insurance or individual and family plans. Employer-sponsored insurance is usually more affordable, as employers often cover a portion of the premium costs. Individual and family plans, on the other hand, can be purchased directly from insurance companies or through the Health Insurance Marketplace. Public health insurance is provided by the government and includes programs like Medicaid, Medicare, and the Children's Health Insurance Program (CHIP). Medicaid offers coverage for low-income individuals and families. Medicare primarily serves people aged 65 and older, as well as certain younger individuals with disabilities. CHIP provides coverage for children in families that earn too much to qualify for Medicaid but cannot afford private insurance. International health insurance is designed for individuals traveling or residing in foreign countries. Expatriate health insurance offers comprehensive coverage for those living abroad long-term, while travel health insurance provides temporary coverage for medical emergencies during trips. Understanding the components of a health insurance plan is essential for making informed decisions and selecting the best coverage for one's needs. These components include premiums, deductibles, copayments and coinsurance, and out-of-pocket maximums. Premiums are the monthly payments made by individuals to maintain their health insurance coverage. The cost of premiums can vary based on factors such as age, location, plan type, and tobacco use. It is essential to consider both the affordability and the coverage offered when selecting a health insurance plan. A deductible is the amount an individual must pay for covered healthcare services before the insurance plan begins to pay. Deductibles can vary between plans and may affect the overall cost of the insurance. High-deductible plans often have lower premiums but require more out-of-pocket expenses before coverage kicks in. Copayments and coinsurance are cost-sharing mechanisms in health insurance plans, where the insured pays a portion of the medical expenses. Copayments are fixed amounts paid for specific services, while coinsurance is a percentage of the total cost. These expenses help control healthcare costs and encourage responsible healthcare utilization. The out-of-pocket maximum is the most an individual will have to pay for covered health care services in a plan year. After reaching this limit, the insurance plan will cover 100% of the costs for the rest of the year. Out-of-pocket maximums help protect individuals from exorbitant medical expenses and provide a sense of financial security. Selecting the right health insurance plan involves assessing one's needs and budget, comparing insurance providers, understanding plan benefits and limitations, and evaluating network providers. To choose the best health insurance plan, individuals must evaluate their healthcare needs and financial situation. This includes considering factors such as the frequency of medical visits, pre-existing conditions, and the affordability of premiums, deductibles, and out-of-pocket maximums. It is essential to compare different health insurance providers to determine which one offers the best coverage at the most affordable price. Researching customer reviews and satisfaction ratings can provide valuable insights into the quality of services and customer support offered by the insurer. Before selecting a health insurance plan, individuals must carefully review the benefits and limitations of each plan. This includes understanding covered services, prescription drug coverage, and any exclusions or restrictions that may apply. A thorough examination of the plan documents can help avoid unexpected costs and ensure adequate coverage. Health insurance plans often have networks of healthcare providers that offer services at negotiated rates. It is crucial to check if one's preferred doctors, hospitals, and specialists are included in the plan's network, as receiving care from out-of-network providers may result in higher out-of-pocket expenses. Several laws and regulations govern health insurance in the United States, including the Affordable Care Act (ACA), Health Insurance Portability and Accountability Act (HIPAA), and Consolidated Omnibus Budget Reconciliation Act (COBRA). The ACA, also known as Obamacare, is a federal law enacted in 2010 that aims to improve the accessibility, affordability, and quality of health insurance. The ACA introduced several reforms, such as prohibiting insurers from denying coverage due to pre-existing conditions and allowing young adults to remain on their parents' insurance plans until age 26. HIPAA is a federal law passed in 1996 that protects the privacy of individuals' health information and establishes standards for the electronic exchange of healthcare data. HIPAA also ensures that individuals can maintain their health insurance coverage when changing jobs, provided they meet certain eligibility criteria. COBRA is a federal law that allows eligible employees and their dependents to continue their health insurance coverage temporarily after losing it due to certain life events, such as job loss or divorce. COBRA coverage can be expensive, as individuals must pay the full premium cost without employer contributions. Health insurance has a significant impact on healthcare by providing access to healthcare services, promoting preventive care and early detection, and offering financial protection against medical expenses. Health insurance improves access to healthcare services by enabling individuals to seek medical care without worrying about the cost. This helps prevent delays in treatment and ensures that individuals can receive the care they need when they need it. By covering preventive services, such as vaccinations and screenings, health insurance promotes early detection of diseases and helps individuals maintain good health. Early detection can lead to more effective treatments, better outcomes, and reduced healthcare costs in the long run. Health insurance provides financial protection by covering a portion of medical expenses, reducing the risk of medical debt and bankruptcy. This allows individuals to focus on their health and well-being, rather than worrying about the financial burden of medical bills. The health insurance industry faces several challenges and is continually evolving to adapt to new trends. Some of these challenges include rising healthcare costs, disparities in health insurance coverage, telemedicine and technological advancements, and policy changes and healthcare reform. One of the most significant challenges facing the health insurance industry is the rising cost of healthcare. Factors contributing to this increase include high prescription drug prices, expensive medical treatments, and an aging population. Insurers must find ways to balance the need for comprehensive coverage with the affordability of premiums and other plan components. Despite efforts to expand health insurance coverage, disparities remain among different population groups. Factors such as income, race, and geographic location can influence an individual's ability to access affordable health insurance. Addressing these disparities is critical to ensuring that all individuals have equal access to healthcare services. Telemedicine and other technological advancements are changing the way healthcare is delivered and accessed. Health insurance companies must adapt to these changes by incorporating new technologies into their coverage options, ensuring that policyholders can benefit from innovative healthcare solutions. The health insurance landscape is continually evolving due to policy changes and healthcare reform efforts. Insurers must stay informed of these changes and adjust their offerings accordingly to remain competitive and compliant with regulations. Health insurance plays a vital role in society by providing individuals with access to necessary healthcare services and offering financial protection against high medical expenses. By understanding the various aspects of health insurance, individuals can make informed decisions about their coverage options and advocate for improvements and innovations within the industry. Furthermore, addressing the challenges and embracing new trends in health insurance will help ensure that everyone has the opportunity to access affordable, quality healthcare.What Is Health Insurance?

Health Insurance Coverage Options

Private Health Insurance

Public Health Insurance

International Health Insurance

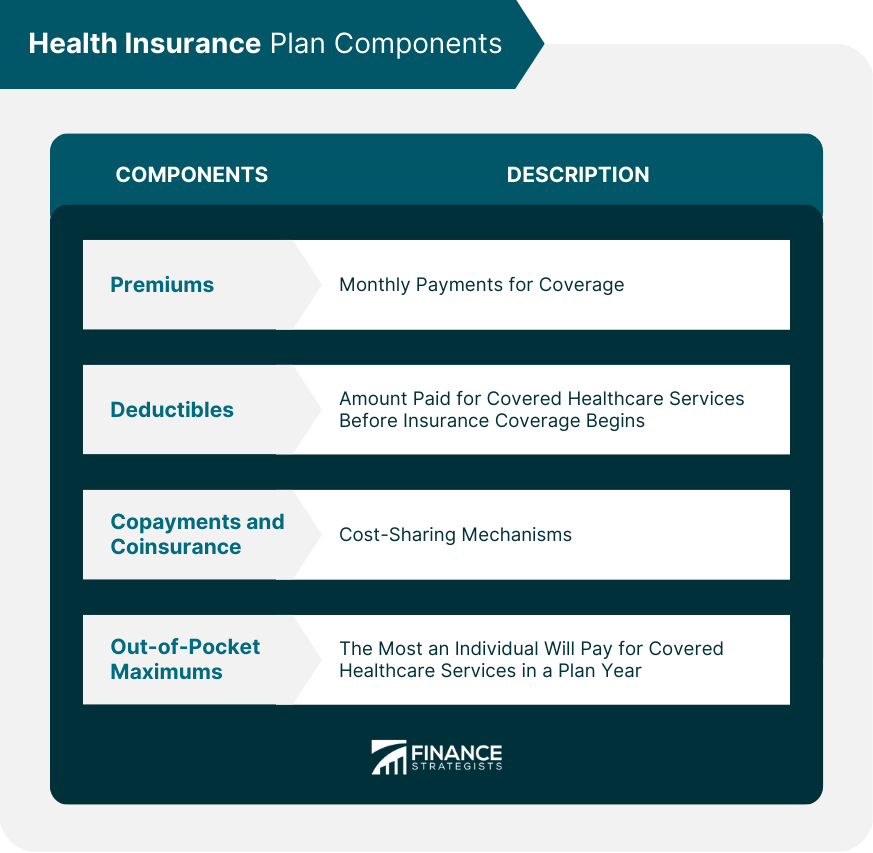

Health Insurance Plan Components

Premiums

Deductibles

Copayments and Coinsurance

Out-of-Pocket Maximums

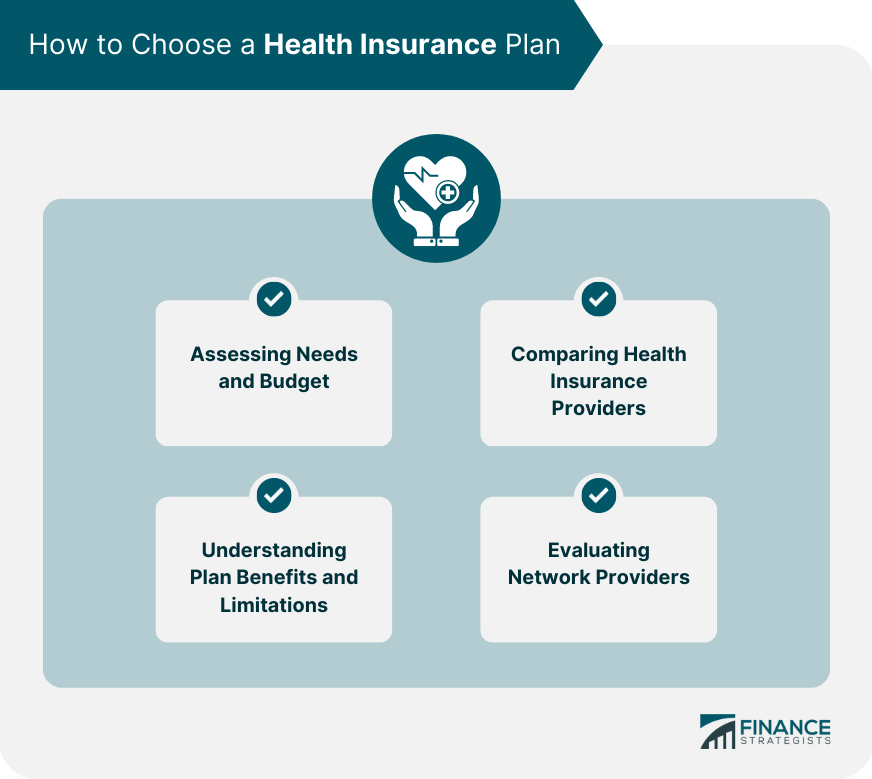

Choosing a Health Insurance Plan

Assessing Needs and Budget

Comparing Health Insurance Providers

Understanding Plan Benefits and Limitations

Evaluating Network Providers

Laws and Regulations Governing Health Insurance

The Affordable Care Act (ACA)

Health Insurance Portability and Accountability Act (HIPAA)

Consolidated Omnibus Budget Reconciliation Act (COBRA)

The Impact of Health Insurance on Healthcare

Access to Healthcare Services

Preventive Care and Early Detection

Financial Protection and Reduced Medical Debt

Challenges and Future Trends in Health Insurance

Rising Healthcare Costs

Disparities in Health Insurance Coverage

Telemedicine and Technological Advancements

Policy Changes and Healthcare Reform

Conclusion

Health Insurance FAQs

Health insurance is a type of insurance coverage that pays for medical and surgical expenses incurred by the insured person.

There are various types of health insurance such as individual health insurance, group health insurance, Medicare, Medicaid, and more.

Health insurance typically covers medical expenses, hospitalization costs, prescription drugs, and preventive care. However, coverage varies based on the type of plan.

In some countries, health insurance is mandatory, while in others, it is optional. However, having health insurance is strongly recommended to protect yourself from unexpected medical expenses.

When choosing a health insurance plan, consider the coverage options, costs, network of healthcare providers, and your personal health needs. It's best to compare plans and ask for expert advice.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.