Property and casualty insurance is a vital component in the financial well-being of individuals, businesses, and communities. It provides protection against a wide range of risks, ensuring financial stability and peace of mind. Property and casualty insurance is a type of insurance coverage that protects individuals and businesses from financial losses resulting from damage to their property or liability for injuries and damages caused to others. This type of insurance is designed to safeguard policyholders against unexpected events and ensure that they can recover from financial setbacks. Property and casualty insurance is essential because it allows individuals and businesses to protect their assets, minimize financial losses, and maintain their standard of living or operations following an unexpected event. It also helps to create a more stable and resilient society by spreading the financial risk associated with accidents, natural disasters, and other unforeseen events. Property and casualty insurance can be broadly categorized into personal lines and commercial lines. Personal lines are designed to cover individuals and families, while commercial lines are tailored for businesses and organizations. Homeowners insurance provides coverage for damage to a policyholder's home and personal property, as well as liability coverage for injuries or damages caused to others on their property. This type of insurance is essential for homeowners, as it helps them recover from disasters and accidents and provides financial protection against potential lawsuits. Renters insurance covers the personal belongings of tenants living in a rented property. It also provides liability coverage for injuries or damages caused to others within the rented premises. Renters insurance is important for tenants, as it ensures that their personal belongings are protected and that they have financial protection against potential liability claims. Condominium insurance is a specialized type of property and casualty insurance designed for condo owners. It covers the personal property of the owner, as well as any improvements made to the unit, and provides liability coverage for injuries or damages occurring within the unit. Condominium insurance is crucial for condo owners, as it helps protect their investment and safeguards them against potential lawsuits. Automobile insurance covers drivers and their vehicles against damages and liability resulting from accidents, theft, and other events. This type of insurance is mandatory in most states and helps ensure that drivers can cover the costs associated with accidents and other incidents on the road. Commercial property insurance covers businesses for damages to their buildings, equipment, and inventory resulting from events such as fires, storms, and theft. This type of insurance is essential for businesses, as it helps them recover from disasters and continue their operations with minimal disruption. General liability insurance provides coverage for businesses in case they are found responsible for causing injuries or damages to third parties. This type of insurance is critical for businesses, as it protects them from potential lawsuits and the financial consequences of liability claims. Business interruption insurance compensates businesses for lost income and additional expenses resulting from a covered event that disrupts their operations, such as a fire or natural disaster. This type of insurance is important for businesses, as it helps them maintain their financial stability during periods of disruption and recovery. Workers' compensation insurance covers employees for medical expenses and lost wages resulting from work-related injuries or illnesses. This type of insurance is mandatory in most states and is crucial for businesses, as it protects them from potential lawsuits and ensures that their employees receive the necessary support to recover and return to work. Commercial auto insurance covers businesses for damages and liability resulting from accidents involving their company vehicles. This type of insurance is essential for businesses that rely on vehicles for transportation, deliveries, or other work-related purposes, as it helps protect them from financial losses and potential lawsuits. Property and casualty insurance operates on a set of core principles that guide the underwriting, pricing, and claims processes. These principles are essential for ensuring that insurance companies can provide coverage while maintaining their financial stability. Insurable interest refers to the financial stake a policyholder has in the subject of insurance. A person or business must have an insurable interest in the insured property or liability to be able to obtain insurance coverage. This principle ensures that insurance is only used to protect genuine financial interests, preventing fraud and speculative practices. Indemnity is the principle that insurance should only compensate policyholders for the actual financial loss they have suffered. This prevents policyholders from profiting from insurance claims and encourages them to take steps to prevent or mitigate losses. Indemnity is a fundamental concept in property and casualty insurance, as it helps maintain the integrity of the insurance system. Subrogation is the process by which an insurance company assumes the legal rights of a policyholder to pursue recovery from a third party responsible for the insured loss. This principle allows insurance companies to recoup their claim payouts from responsible parties, helping to maintain the financial stability of the insurance system and ensuring that costs are distributed fairly. Contribution is the principle that, when multiple insurance policies cover the same risk, each insurer should contribute to the payment of a claim proportionately. This prevents policyholders from receiving double compensation for their losses and ensures that the financial burden of claims is shared equitably among insurance companies. Proximate cause is the principle that insurance coverage should only apply when the insured event is the direct and immediate cause of the loss. This helps to establish the scope of coverage and determine whether a particular loss is covered under the policy. Proximate cause is an essential concept in property and casualty insurance, as it helps to define the boundaries of insurance protection. Deductibles are the portion of a claim that policyholders must pay before their insurance coverage kicks in. Deductibles are used to discourage small or frivolous claims, encourage policyholders to take preventive measures, and reduce the overall cost of insurance. Deductibles are a common feature of property and casualty insurance policies and play a crucial role in managing insurance costs. The claims process is an essential aspect of property and casualty insurance, as it determines how policyholders are compensated for their losses. This process involves several key steps, from reporting a claim to receiving a settlement. When a loss occurs, policyholders must report the claim to their insurance company as soon as possible. Timely reporting is crucial, as it allows the insurer to begin the investigation and adjustment process and helps ensure that the claim is handled efficiently and fairly. Once a claim is reported, the insurance company assigns a claims adjuster to investigate the circumstances of the loss and determine the extent of the damages. The adjuster's role is to verify the details of the claim, assess the policyholder's coverage, and calculate the amount of the settlement based on the policy provisions and the principle of indemnity. After the investigation and adjustment process, the insurance company will offer a settlement to the policyholder, which represents the amount they are willing to pay for the covered loss. The policyholder can either accept the settlement or negotiate for a higher amount if they believe the offer is insufficient. Once an agreement is reached, the insurance company will issue a payment to the policyholder or directly to the parties involved in the loss, such as repair shops or medical providers. In some cases, policyholders may disagree with the insurance company's decision regarding their claim. They may believe that their claim was unfairly denied, or that the settlement offered is too low. In such cases, policyholders can appeal the decision, providing additional evidence or seeking the assistance of a claims advocate or legal professional to help resolve the dispute. Property and casualty insurance is regulated at both the state and federal levels to ensure the stability, fairness, and transparency of the industry. Each state has its own insurance department responsible for overseeing the licensing, financial solvency, and market conduct of insurance companies operating within their jurisdiction. State insurance departments also handle consumer complaints and enforce state insurance laws and regulations. The National Association of Insurance Commissioners (NAIC) is a voluntary organization of state insurance regulators that promotes coordination and cooperation among state insurance departments. The NAIC develops model laws, regulations, and best practices to help harmonize state insurance regulations and facilitate the efficient operation of the insurance industry. While the primary responsibility for regulating property and casualty insurance lies with the states, the federal government plays a limited role in certain areas. These include overseeing the National Flood Insurance Program (NFIP) and providing reinsurance for terrorism-related losses through the Terrorism Risk Insurance Act (TRIA). The property and casualty insurance industry is constantly evolving in response to technological advancements, changing risk landscapes, and shifting consumer expectations. Insurtech refers to the use of technology to enhance the efficiency, accessibility, and affordability of insurance products and services. From artificial intelligence and machine learning to blockchain and mobile applications, insurtech innovations are transforming the property and casualty insurance industry by streamlining operations, improving underwriting and pricing accuracy, and enhancing the customer experience. Telematics is the use of wireless devices and communication technology to collect and transmit data on vehicle usage, driving behavior, and other factors relevant to insurance risk assessment. Telematics is particularly prominent in the auto insurance sector, where it enables usage-based insurance (UBI) and other innovative pricing models that reward safe driving and promote risk mitigation. Climate change is increasing the frequency and severity of natural disasters, leading to greater volatility and unpredictability in property and casualty insurance claims. Insurers are increasingly relying on advanced catastrophe modeling and data analytics to better understand and manage the risks associated with climate change and extreme weather events. As businesses and individuals become more reliant on digital technology, the risk of cyberattacks and data breaches is growing. Cyber insurance is a rapidly emerging segment of the property and casualty insurance market, offering coverage for financial losses resulting from cyber incidents and helping policyholders navigate the complex and evolving landscape of cybersecurity risks. The sharing economy, characterized by peer-to-peer platforms and on-demand services such as ridesharing and home-sharing, is creating new challenges and opportunities for property and casualty insurers. As traditional risk profiles change and new exposures emerge, insurers must adapt their products and services to meet the unique needs of the sharing economy. Understanding property and casualty insurance is essential for individuals and businesses looking to protect their assets, mitigate financial risks, and maintain their standard of living or operations in the face of unexpected events. By staying informed about the types, principles, and processes involved in property and casualty insurance, as well as current trends and challenges in the industry, policyholders can make informed decisions about their coverage and ensure they have the protection they need. As the property and casualty insurance industry continues to evolve, it is crucial for both insurers and policyholders to adapt to emerging risks, technological advancements, and changing market dynamics. By doing so, they can ensure the ongoing stability and resilience of the insurance system, providing a vital safety net for individuals, businesses, and communities alike.What Is Property and Casualty Insurance?

Types of Property and Casualty Insurance

Homeowners Insurance

Renters Insurance

Condominium Insurance

Automobile Insurance

Commercial Property Insurance

General Liability Insurance

Business Interruption Insurance

Workers' Compensation Insurance

Commercial Auto Insurance

Principles of Property and Casualty Insurance

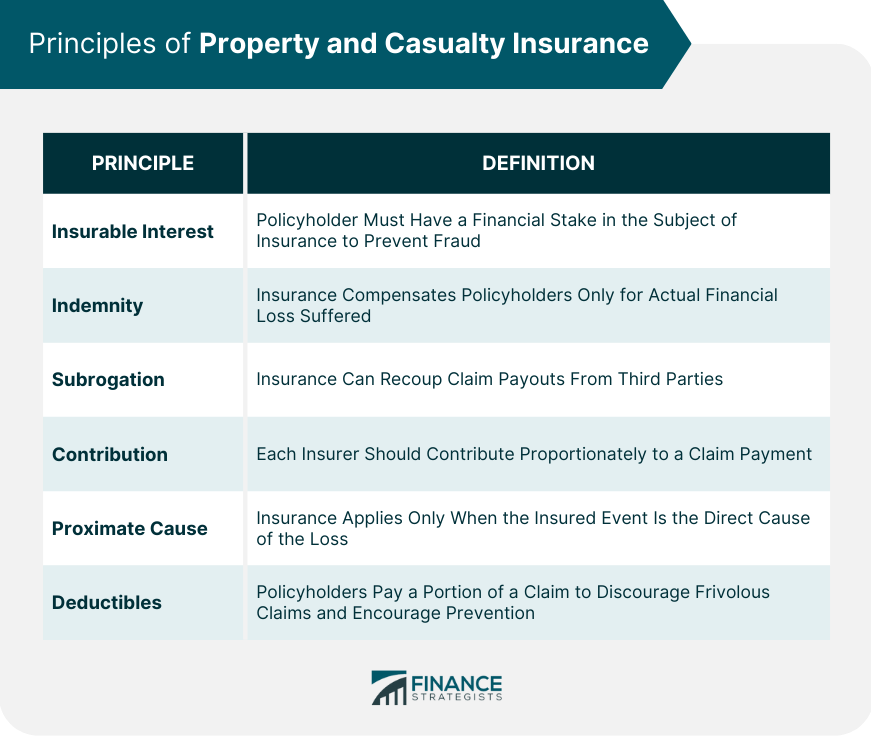

Insurable Interest

Indemnity

Subrogation

Contribution

Proximate Cause

Deductibles

Insurance Claims Process

Reporting a Claim

Investigation and Adjustment

Settlement and Payment

Claims Disputes and Appeals

Regulation of Property and Casualty Insurance

State Insurance Departments

National Association of Insurance Commissioners (NAIC)

Federal Involvement in Property and Casualty Insurance

Emerging Trends and Challenges

Technological Advancements

Climate Change and Catastrophe Modeling

Cyber Insurance

The Sharing Economy

Conclusion

Property and Casualty Insurance FAQs

Property and Casualty insurance is a type of insurance that protects individuals and businesses from losses or damages to their property, belongings, or assets due to unexpected events such as theft, fire, or natural disasters.

The types of insurance that fall under Property and Casualty insurance include home insurance, auto insurance, business insurance, liability insurance, and renters insurance, among others.

Property and Casualty insurance is essential because it helps protect your assets and mitigate risks. Without this insurance, you could face significant financial losses due to unforeseen events.

The cost of Property and Casualty insurance varies depending on several factors, such as the type of coverage, the value of your assets, your location, and your claims history.

To find the right Property and Casualty insurance for your needs, it's essential to evaluate your assets and risks and compare quotes from different insurers. You can also seek advice from an insurance agent or broker to help you choose the best coverage.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.