Insurance is an agreement represented by a policy, under which an individual or corporation receives financial protection or payment from an insurer in the event of a loss. The company pools clients' risks to make funds available to pay for the claims. People obtain insurance not only to reduce risks posed by unforeseen occurrences but also to assist with common expenses, such as annual medical checkups and dentist appointments. Moreover, insurance firms negotiate discounts with healthcare providers, and their clients pay the discounted rates. The most challenging aspect of insurance is paying for something you hope you never need. Nobody wants anything unpleasant to happen to them. However, if you experience a loss without insurance, you may be in a precarious financial situation. When you purchase insurance, you contract with an insurer. In the insurance contract, you agree to pay premiums to the insurer in exchange for protection against covered losses. Additionally, you consent to abide by the conditions of the insurance contract, such as giving the insurer notice of a loss within a specified period. Then, you can let the firm inspect the property before repairs are done. A good rule of thumb is that if your damages are less than your deductible, it is usually not worth submitting a claim for a relatively modest payout. If you have a claim, you must submit documentation, such as a police report or medical bills, to the insurer. The insurance company then pays for covered losses according to the terms of your policy. Distinct forms of insurance, like auto and home, have different policies that cover force majeure. While homeowners insurance can offer protection against various natural calamities, it may sometimes refer to a comprehensive auto insurance policy for vehicles. Consider the case where you have homeowners insurance. In that instance, it will probably cover theft, wind, hail, lightning, and fire damage. It also covers losses brought on by outside events, such as a tree collapsing. If you own a vehicle, you are obliged by law to carry auto insurance. Some insurance is contractual, such as building insurance for a mortgage. In contrast, others, such as life insurance and retirement savings, are practical. Most insurance firms create revenue in two ways: first, by charging premiums to their customers in exchange for insurance coverage, and second by reinvesting those premiums into other interest-generating assets. Insurance is important for the following reasons: The insured's risk of loss is transferred to the insurer through insurance. The underlying premise of insurance is to distribute risk among many individuals. The majority of the population purchases insurance and pays premiums to the insurer. Whenever a loss happens, it is reimbursed by funds collected from millions of policyholders. When an unforeseen event, such as death, disability, critical illness, or property damage, insurance provides the financial safety and security needed to cope with the situation. Insurance gives policyholders peace of mind and protection from catastrophic losses. Insurance policies are long-term contracts. The premiums paid today to create a financial asset that will be there when policyholders need it in the future. Insurance companies invest the premiums in a variety of assets, such as stocks, bonds, and real estate, which generate additional income that can be used to pay claims. Some insurance policies may guarantee a reliable income source after retirement. The importance of insurance in post-retirement life will depend on your current investment strategy. The insurance industry produces revenue from premiums paid by millions of policyholders. These funds are used to build long-lasting national infrastructure (such as roads, ports, power plants, and dams) because of their long-term nature. Large investments leading to the development of capital in the economy boost employment chances. Additionally, insurance facilitates loss reduction, financial stability, and the promotion of trade and commerce activities, all of which contribute to sustained economic growth and development. Medical emergencies can happen anytime and often result in financial hardship. Insurance gives the policyholder access to quality medical care without worrying about the cost. In the case of a medical emergency, insurance pays for hospitalization, surgical procedures, diagnostic tests, and other treatments. Insurance also covers pre-existing conditions and preventive care. Insurance has three components: premium, policy limit, and deductible. Understanding them will help you choose the right policy. A policy's premium is the amount you pay your insurer regularly to maintain coverage. You may be able to pay your premiums monthly, quarterly, semiannually, or annually depending on your insurance provider and coverage. You will no longer be covered if your insurance premium is not paid during the grace period. Nevertheless, depending on your insurer's reinstatement policies, your insurance may be reinstated. An insurance company determines the premium for an insurance plan based on various factors. The objective is to assess whether or not an insured individual is eligible for the sort of insurance plan they wish to acquire. The policy limit is defined as the maximum obligation of an insurance company for damages covered by the policy. It is determined based on the insurance period, loss or damage, and other equivalent factors. In general, the higher the policy limit, the higher the premium. The face value of a general life insurance policy refers to the highest amount the insurer will pay upon the insured's death. A deductible is the amount or proportion of a claim the insured agrees to pay out of pocket before the insurer begins to pay. The insurance company is solely responsible for paying the claim amount if it exceeds the deductible. Deductibles are defined by the terms of a specific policy type and apply per policy or claim. Due to the higher out-of-pocket expense, insurance policies with high deductibles are often less expensive because fewer claims are filed. It can be a fixed cash payment or a percentage of the entire insurance coverage provided by a policy. On the declarations page of typical homeowners, renters, and vehicle insurance policies, you can find the terms of your coverage, which determine the amount. There are many different types of insurance, each with its specific coverage. The most common types of insurance are: Life Insurance is a contract between an insurance policyholder and an insurer in which the insurer agrees to pay a sum of money to the beneficiary upon the insured person's death or after a predetermined period. This benefit comes in exchange for the policyholder's premium payments. Life insurance safeguards the future of your loved ones by paying a lump payment, known as a death benefit, in the case of an unfortunate incident. Health insurance is a type of insurance that pays for the policyholder's medical and surgical costs. It is designed to cover health care costs, including hospitalization, doctor visits, prescription drugs, and more. Most health insurance plans also provide coverage for preventive care, such as vaccinations and screenings. Depending on the individual's health insurance coverage, the insured pays out-of-pocket and is reimbursed, or the insurer pays the provider directly. In countries lacking universal healthcare coverage, employer benefits packages typically include health insurance. Long-term disability insurance (LTD) ensures that employees continue to receive a portion of their income if they are out of work for an extended period due to a covered disability. These absences may result from work-related or non-work-related accidents, injuries, or illnesses. Disability insurance is sometimes known as income replacement insurance since it pays benefits to replace a portion of your lost income if you cannot work due to a long-term illness or injury. You will continue to receive benefits until you can return to work or until your benefit period expires. If anything unforeseen, such as a fire or burglary, occurs, your homeowner's insurance will cover the resulting losses and damages to your property. When you have a mortgage, your lender will require you to get property insurance. For this reason, mortgage lenders typically request documentation of homeowner's insurance. Auto insurance is a specific kind of policy that offers financial compensation for the repercussions that arise if your vehicle is involved in an accident. Car insurance rating tiers are a relatively new concept that allows drivers to obtain various prices based on many pieces of personal information. It is crucial to note that each insurer has its unique tier structure and calculation, so do your homework before accepting the coverage. There are various tiers of coverage available in addition to the minimum liability coverage mandated by most states. These tiers give additional coverage for a wide variety of potential damages. Travel insurance is a type of insurance coverage intended to protect against the dangers of traveling and any financial losses that may occur as a result of those dangers. The potential consequences range from minor inconveniences, such as missing a flight connection or having luggage delivered late, to significantly more serious problems, such as acute illness or injury. Insurance policies typically have five main parts: The declaration page is the first page of your insurance policy and includes your name, address, policy number, and the effective dates of your coverage. It also specifies the premium amount, coverage limits, deductible amounts, endorsements, and applied discounts. On the declaration page, specific assets covered by an insurance policy, such as a home or personal property, would also be specified. The insuring agreement is the section of the policy in which the insurer expressly agrees to indemnify the covered party. This section includes who and what is covered in the insurance contract and what are the insurer's responsibilities to the insured. The form of the insurance contract can vary based on the type of insurance coverage. For instance, the contract should include coverage for named perils if you purchase homeowner's insurance. If an incident is listed under the named-perils coverage, then the policy covers it. Typically specified perils for homeowner's insurance include fire and lightning damage. If a peril is not listed in the insurance contract, it is not covered by the policy. All-risk coverage is distinct. Except for expressly excluded damages, all losses are covered by the policy under this sort of insurance contract. Life insurance is an example of all-risk coverage. Exclusions convey to the insured what is not covered by the insurance policy. The three main types of exclusions include: This section also emphasizes the insurance contract's limitations and conditions. Limitations refer to the policy limits, such as the highest amount an insurer will pay for a specific loss. Conditions are the obligations of the insured, such as timely payment of premiums and notification of losses. If the insured does not meet these standards, the insurance provider maintains the right to deny the claim. Riders are modifications to the coverage. The modification of a health insurance policy's level of benefits is an example of a rider. When a policy is renewed, an insurer may alter the language or coverage of the policy. Changes to an insurance policy are typically communicated to the insured party by the insurance company. The definitions clause clarifies all of the terminology used in the policy to ensure that there is no room for ambiguity and that the insured is aware of all aspects of the coverage. It could be an independent section or a subsection. When choosing an insurance policy, it is important to consider the type and amount of coverage you need and the deductible amount. It would help if you also compare different policies to find the one that best suits your needs. There are a few things to remember when choosing an insurance policy. The type of coverage you need: Many different types of insurance policies are available. Ensure that you select the option that best meets your needs. If preserving your family's financial security is your main goal, you may be able to find a term insurance plan that offers extensive coverage at reasonable costs. If you are attempting to save money for your child's education or hoping to purchase your dream home, you might want to consider investing in a unit-linked insurance plan. You can also buy a retirement plan that will provide a steady income for your ongoing living expenses once you retire. The amount of coverage you need: You should consider the value of your assets and how much coverage you would need to protect them. The deductible amount: You must pay out-of-pocket as a counterpart for the loss or damage claim. Higher deductibles typically result in lower premiums. The guaranteed savings: Check how much guaranteed savings you will receive if you are looking for an insurance plan with an investment component. Examine each policy alternative to determine the length of time you will be locked in and the guaranteed savings amount. You will also need to know if the policy allows access to your funds anytime or if they are unavailable until the policy's maturity date. The price: Insurance policies can vary widely in price. Compare different policies to find the best fit for your budget. Banks and insurance businesses contribute to economic progress and savings promotion. Still, they do it very differently and offer their respective customer bases different promises. When it comes to choosing between a bank and an insurance company, it is important to weigh your options and choose the institution that best suits your needs. Insurance is a contract, represented by a policy, in which an individual or entity receives financial protection or compensation against losses from an insurer. The insured is the individual or entity who purchases the insurance policy. The insurer agrees to pay the insured for certain covered losses as specified in the insurance policy. Insurance is designed to protect an individual, company, or other entity's financial well-being in case of unexpected loss. Many different types of insurance exist, including health, life, auto, homeowner's, and travel insurance. Comparing prices, coverage options, deductible amounts, and guaranteed savings are important when choosing an insurance policy. Insurance policies are often complex and may contain exceptions and limitations. It is important to understand a policy's terms and conditions before buying it. An insurance broker can provide you with a more personalized approach to meet your financial goals. What Is Insurance?

How Insurance Works

Importance of Insurance

Spreads Large Risks

Provides Financial Safety and Security

Generates Long-Term Wealth

Builds Economic Development

Provides Support During Medical Emergencies

Components of Insurance

Premium

Policy Limit

Deductible

Types of Insurance

Life Insurance

Health Insurance

Long-Term Disability Insurance

Homeowner's Insurance

Auto Insurance

Travel Insurance

Parts of an Insurance Policy

Declaration Page

Insuring Agreement

Exclusions, Limitations, and Conditions

Riders

Definitions

How to Choose an Insurance Policy

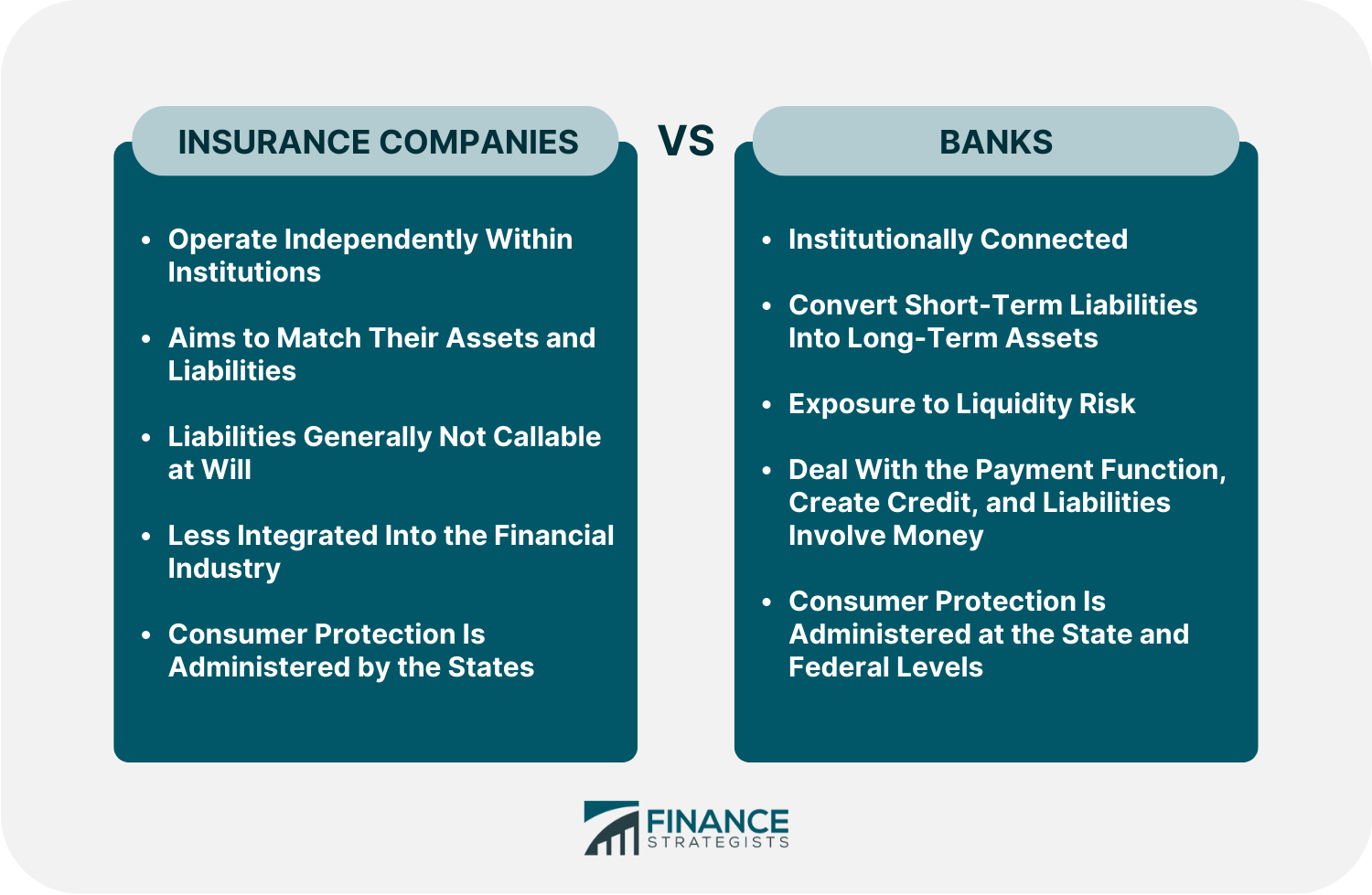

Insurance Companies vs Banks

Final Thoughts

Insurance FAQs

The earlier you purchase life insurance, the better the timing will be. You will be eligible for lesser rates if you are younger. Additionally, as you become older, you can develop health problems that increase the cost of your insurance or prevent you from being eligible for coverage.

Insurers use deductibles to ensure that policyholders are invested in the outcome and will pay their fair share of any claims. Deductibles lessen the financial burden a catastrophic loss or an unexpected buildup of smaller losses places on an insurer.

There are many different types of insurance, but some of the most common include health, life, auto, homeowner's, and travel insurance.

Insurance coverage refers to the amount of risk or liability covered by insurance services for an individual or organization.

The most obvious and significant benefit of insurance is the payment of losses. A contract, known as an insurance policy, is used to compensate people and organizations for losses covered by the policy.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.