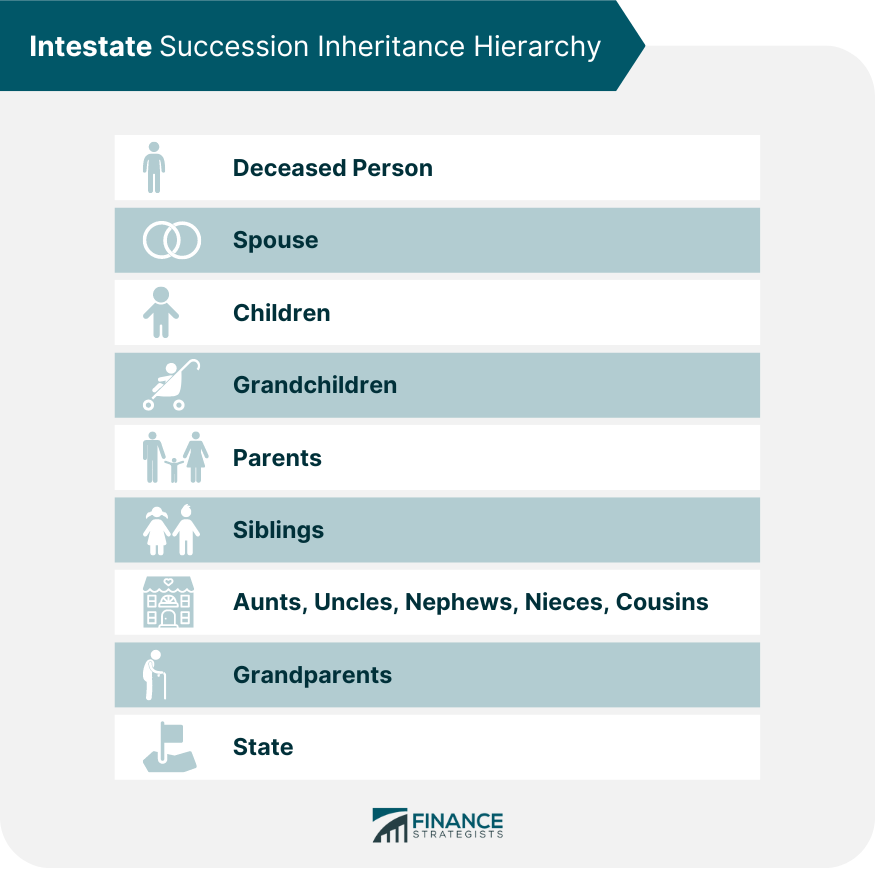

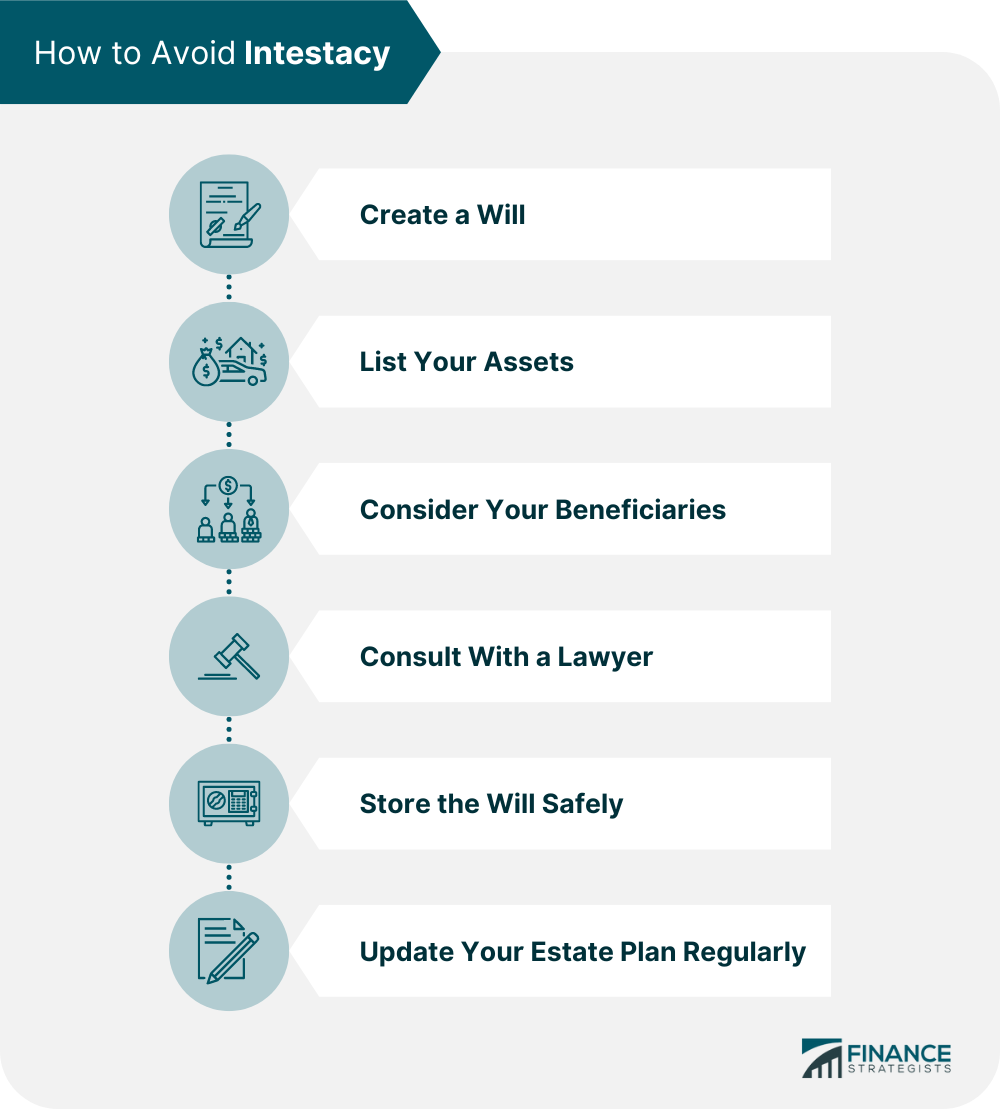

Intestate is a legal term used to describe the state of an individual who passes away without leaving a valid will or when the will presented to a court is deemed invalid. In an intestate, the laws of the state where the death took place will decide how the assets and possessions of the deceased will be divided, usually based on blood or marital relationship. Intestate succession laws vary between states, so it is crucial to understand the specific laws in each state. Additionally, if an individual has dependents, it is highly recommended to consult an estate planning attorney to ensure their assets are distributed accordingly. The probate process applies when an individual passes away without a valid will or dying intestate. The process is designed to distribute the deceased person's assets and property to their rightful heirs. When a person dies intestate, asset and property distribution will be determined by the laws of the state in which they stayed at the time of their death. The probate court in this state will oversee the distribution process. Without a will, the court will appoint an administrator to manage the deceased person's estate. The administrator is responsible for the inventory and valuation of all assets and property belonging to the deceased. The administrator will use the estate's assets to settle debts and taxes the deceased person owes. Once the debts and taxes have been paid, the remaining assets will be distributed to the heirs according to the state's intestate succession laws. Spouses are considered joint owners of any assets acquired during the marriage and are generally entitled to receive at least half of the deceased person's estate in community property states. In states that follow common law, the distribution of assets typically begins with the surviving spouse. The court may determine that the spouse should receive less than half, more than half, or all of the estate if the deceased person had no living children or grandchildren. If the person was unmarried or was a widow or widower when they died, the assets will go to their children first, then to any other relatives. When no living relatives are identified, the estate's assets will fall into the state's ownership in a process known as escheatment. When a person dies without a will, the state's intestate succession laws determine the distribution of their assets and property. In some cases, disputes may arise between family members over the distribution of the deceased person's assets. Such can lead to prolonged legal battles and emotional stress for all parties involved. The probate process can be lengthy and complex and involve significant paperwork resulting in a delayed distribution. Court fees and other expenses associated with the probate process can reduce the amount of assets available for distribution to the heirs. In case of complex family history or relatives being out of touch with each other, locating the deceased’s heirs can be challenging. Intestate succession refers to the laws governing the allocation of a deceased person's assets in the event they die without a valid will. These laws differ for each state but generally follow a hierarchy of eligible heirs. The distribution of assets in an intestate estate begins with the surviving spouse and children. If the deceased person is unmarried or widowed, the assets will be divided among their surviving children. The surviving spouse is typically entitled to at least half of the deceased person's estate. The surviving spouse might inherit the entire estate if the deceased had no living children or grandchildren. Typically, the surviving spouse and children would share the entire estate if they were all still living. If a child of the deceased has passed away, the deceased person's grandchildren would typically inherit their parent's share. If the deceased person has no children, the assets will be passed to their parents or siblings, followed by uncles, aunts, nieces, cousins, nephews, and even grandparents. The assets will become the state's property if no surviving relatives exist. The best way to ensure that your assets are distributed according to your wishes upon your death is to create a legal will. Create a Will. A will is a legally binding document outlining how you would like your assets to be distributed after death. By creating a will, you can avoid the uncertainties and difficulties associated with intestate succession. List Your Assets. Make a list of all your assets, including real estate, personal property, bank accounts, stocks, and life insurance policies. Consider Your Beneficiaries. Identify who you want to receive your assets and how you want your assets to be distributed. You may also want to explore a per stirpes or per capita distribution and see what is most appropriate for you. Consult a Lawyer. Consult with an estate planning lawyer who specializes in estate planning to draft your will. They will ensure that your will is legally binding and meets all your state's requirements. Store the Will Safely. Once your will is complete, safely store it where it can be easily found after your death. It is also advisable to make a copy of the will and give it to your executor. Update Your Estate Plan Regularly. It is generally recommended to update your estate plan following major life events such as marriage, divorce, the birth of a child, the death of a loved one, or when your children reach the age of legal adulthood. Intestate is the legal term for a person who dies without a valid will or whose will is ruled invalid by a court. Distribution will be determined by the state's laws in which they stayed at the time of their death. Such is facilitated through the probate process – the distribution of the deceased person's assets and property to their rightful heirs. The lengthy and complex probate may result in disputes among family members. It can also involve court fees, paperwork, and expenses that reduce the estate's overall value. Additionally, locating the deceased person's heirs may be an issue. Generally, inheritance is passed to the surviving spouse first, followed by any children or descendants. After that, additional family members such as parents, siblings, grandparents, and cousins are included if no other heirs remain. It is recommended to create a legal will to outline and ensure that assets are distributed according to one's wishes. Consult with an estate planning lawyer for estate planning advice. Ensure to regularly review and update the estate plan.What Is Intestate?

The Probate Process if You Die Intestate

Challenges With Intestate Deaths

What Is Intestate Succession?

How to Avoid Intestacy

Final Thoughts

Intestate FAQs

The order of intestate succession determines who will inherit the assets of a person who dies without a valid will. The inheritance hierarchy typically starts with the surviving spouse, then any surviving children and descendants, and then other relatives, such as parents, siblings, grandparents, uncles, aunts, and cousins, if any.

Intestate property is divided according to the laws of the deceased person's state of residence at the time of death. Usually, a court will oversee and determine how assets are distributed among heirs.

Probate is the legal process of dividing a deceased person's assets and property to their rightful heirs. Intestate refers to someone who dies without leaving a valid will, or whose will is ruled invalid by a court.

Intestate is the legal term for a person who dies without a valid will or whose will is ruled invalid by a court.

When someone dies intestate, the court will appoint an executor to manage the estate. The executor’s job is to locate and notify any heirs, collect assets and debts owed to the deceased person, and distribute property and assets according to intestacy laws.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.