Retirement income planning involves preparing for your financial needs during your post-working years. It aims to provide a stable income, allowing you to maintain your desired lifestyle and cover essential expenses. Proper retirement income planning is crucial to ensure financial security, achieve retirement goals, and reduce stress. It enables individuals to make informed decisions about their financial future and adapt to changing needs and circumstances. A comprehensive retirement income plan should include various income sources. This section will explore the different types of income, such as Social Security, pensions, investment income, annuities, and part-time work or business income. Social Security is a government program providing retirement benefits to eligible individuals. It serves as a primary source of income for many retirees, but often it's not enough to cover all expenses. Pensions are employer-sponsored retirement plans that provide a defined benefit based on years of service and salary. They are becoming less common, but those who have access to them can rely on a steady income source during retirement. Investment income is derived from various assets, such as stocks, bonds, mutual funds, and real estate. A well-diversified investment portfolio can generate passive income through dividends, interest, and capital gains. Annuities are financial products offered by insurance companies, designed to provide a guaranteed income stream during retirement. They can be purchased as a lump sum or through a series of payments and can offer various payout options. Some retirees choose to work part-time or start a business to supplement their retirement income. This option can provide additional financial security and a sense of purpose during retirement. There are several strategies to enhance retirement income, such as maximizing Social Security benefits, choosing the right pension plan options, building a diversified investment portfolio, and utilizing tax-advantaged retirement accounts. To maximize Social Security benefits, individuals can delay claiming benefits until their full retirement age or later. This strategy can result in a higher monthly payout and a larger total benefit over time. Selecting the appropriate pension plan options can impact the amount of retirement income received. Choices include lump-sum payouts, joint-and-survivor annuities, and single-life annuities, each with its advantages and disadvantages. A diversified investment portfolio includes a mix of stocks, bonds, and other assets, reducing risk and providing potential growth. Rebalancing the portfolio periodically helps maintain an appropriate asset allocation based on individual risk tolerance and financial goals. Contributing to tax-advantaged retirement accounts, such as traditional and Roth IRAs, 401(k)s, and 403(b) plans, can help reduce taxes and grow retirement savings. Health Savings Accounts (HSAs) also offer tax benefits and can be used to cover medical expenses during retirement. Implementing tax-efficient withdrawal strategies can help retirees minimize their tax burden and maximize their retirement income. These strategies may involve strategically withdrawing from different types of accounts, considering Roth conversions, and taking advantage of tax deductions and credits. Incorporating guaranteed income sources, such as Social Security and annuities, can provide a stable income foundation during retirement. These sources can help mitigate the risk of outliving one's assets and ensure a consistent income stream. Understanding your retirement needs and goals is crucial for effective income planning. This includes estimating retirement expenses, projecting retirement income, and identifying potential income gaps. To estimate retirement expenses, consider basic living expenses, healthcare costs, travel, leisure activities, and other financial goals. It's essential to account for inflation and potential changes in spending habits over time Projecting retirement income involves estimating the income you'll receive from Social Security, pension plans, investments, and part-time work or business income. Accurate projections can help you make informed decisions about your retirement plan. Once you've estimated your expenses and projected your income, you can identify any potential retirement income gaps. Addressing these gaps early in the planning process can help ensure you have enough money saved to maintain your desired lifestyle during retirement. Retirement income planning offers numerous benefits, such as financial security, achieving retirement goals, tax efficiency, and reduced stress. A well-crafted retirement income plan provides financial security, ensuring you have a reliable income source throughout your retirement years. This can help prevent running out of money and maintain your desired lifestyle. Retirement income planning helps you set and achieve your retirement goals, such as traveling, pursuing hobbies, or providing financial support to loved ones. A clear plan enables you to allocate resources effectively and prioritize your objectives. Proper retirement income planning can help minimize taxes by strategically withdrawing from different accounts and utilizing tax-advantaged investment vehicles. This can help maximize your retirement income and preserve your savings. Knowing you have a solid retirement income plan in place can alleviate stress and provide peace of mind. It allows you to focus on enjoying your retirement years instead of worrying about financial matters. Despite its benefits, retirement income planning can present some drawbacks, including complexity, potential for overestimating income, changes in market conditions, and inaccurate expense estimations. Retirement income planning can be complex and time-consuming, especially for individuals with limited financial knowledge. Navigating various income sources, tax implications, and investment options can be challenging. There is a risk of overestimating your retirement income, which can lead to insufficient savings and financial stress. This can result from overly optimistic investment returns or underestimating the impact of inflation on expenses. Market conditions can change, affecting your retirement income plan. Fluctuations in investment returns, interest rates, and economic conditions can impact the value of your assets and the income they generate. It can be challenging to accurately estimate your retirement expenses, as your spending habits and needs may change over time. Underestimating expenses can result in an insufficient retirement income, while overestimating can lead to unnecessary sacrifices. Protecting retirement income involves managing various risks and ensuring that one's assets and income streams are safeguarded. Insurance plays a crucial role in protecting retirement income. Health, long-term care, and life insurance policies can help manage potential risks and provide financial security for retirees and their families. Estate planning is essential for protecting one's assets and ensuring a smooth transition of wealth to beneficiaries. This process may include creating wills, and trusts, and updating beneficiary designations. Inflation can erode the purchasing power of retirement income over time. Inflation protection strategies, such as investing in inflation-adjusted annuities or Treasury Inflation-Protected Securities (TIPS), can help preserve the value of one's assets and income. Having contingency plans in place for unforeseen events, such as market downturns or health issues, can help protect retirement income and ensure financial security. These plans may involve adjusting withdrawal strategies, reallocating assets, or seeking additional income sources. It is essential to regularly monitor and adjust one's retirement income plan to account for changing circumstances and market conditions. Regularly reviewing one's retirement income plan can help identify areas for improvement, ensure that the plan remains aligned with financial goals, and allow for necessary adjustments. As circumstances and market conditions change, it is vital to adjust retirement income strategies accordingly. This may involve rebalancing one's investment portfolio, revisiting withdrawal strategies, or updating insurance coverage. Regularly reviewing and updating estate planning documents and beneficiary designations ensures that one's wishes are accurately reflected and that assets are protected for the intended beneficiaries. Retirement income planning is essential for achieving a secure and comfortable retirement. By proactively addressing potential income gaps, diversifying income sources, and working with a qualified financial advisor, you can ensure financial stability and peace of mind. Remember, it's never too early to start planning for your retirement, and the more time you dedicate to this process, the better prepared you will be for a fulfilling and worry-free post-working life. Starting your retirement income planning early allows you to take advantage of compounding returns and make adjustments as needed. Proactive planning ensures you have enough time to build a solid financial foundation and meet your retirement goals. Effective retirement income planning requires balancing risks and rewards. This involves diversifying your investment portfolio, managing withdrawal strategies, and understanding the potential impact of market fluctuations on your retirement income. Your financial needs and goals may change over time, and your retirement income plan should adapt accordingly. Regularly reviewing and updating your plan ensures it remains aligned with your evolving objectives and circumstances. A well-executed retirement income plan can help you achieve a secure and comfortable retirement. By understanding your needs, diversifying your income sources, and making informed decisions, you can enjoy your retirement years with confidence and peace of mind.What Is Retirement Income Planning?

Types of Retirement Income Sources

Social Security

Pensions

Investment Income

Annuities

Part-Time Work or Business Income

Strategies for Retirement Income Planning

Maximizing Social Security Benefits

Choosing the Right Pension Plan Options

Building a Diversified Investment Portfolio

Tax-Advantaged Retirement Accounts

Tax-Efficient Withdrawal Strategies

Guaranteed Income Sources

Assessing Retirement Needs and Goals

Estimating Retirement Expenses

Projecting Retirement Income

Identifying Retirement Income Gap

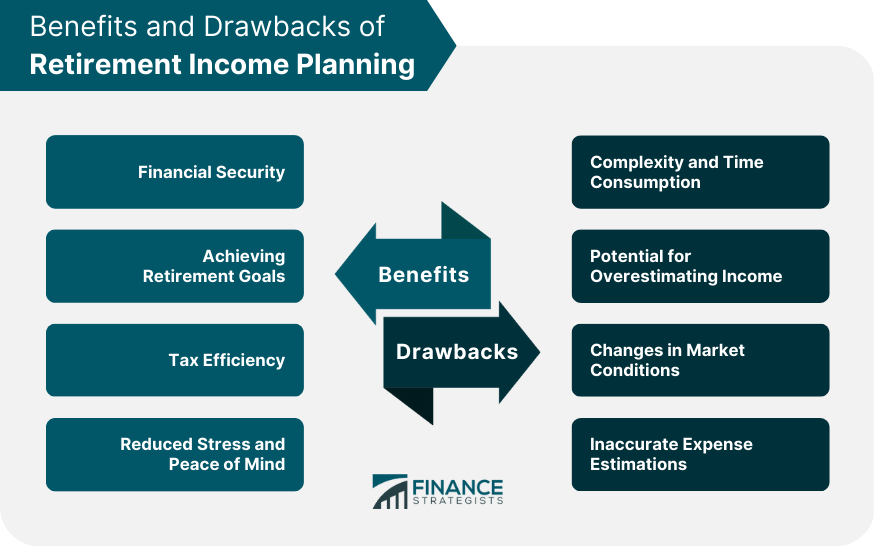

Benefits of Retirement Income Planning

Financial Security

Achieving Retirement Goals

Tax Efficiency

Reduced Stress and Peace of Mind

Drawbacks of Retirement Income Planning

Complexity and Time Consumption

Potential for Overestimating Income

Changes in Market Conditions

Inaccurate Expense Estimations

Protecting Retirement Income

Managing Risks Through Insurance

Estate Planning

Inflation Protection Strategies

Contingency Plans for Unforeseen Events

Regular Monitoring and Adjustments of Retirement Income Planning

Periodic Reviews of Retirement Income Plan

Adjusting Strategies Based on Changing Circumstances and Market Conditions

Updating Estate Planning Documents and Beneficiaries

Final Thoughts

Retirement Income Planning FAQs

Retirement income planning is the process of determining how much money you will need to live comfortably during retirement and creating a plan to ensure that you have enough income to meet those needs.

Some types of retirement income include Social Security benefits, pensions, investment income, and rental income.

Retirement income strategies may include delaying Social Security benefits, managing expenses, diversifying investments, and creating a withdrawal plan from retirement savings.

Retirement income planning can help you achieve financial security during retirement, reduce stress and anxiety, and ensure that you can maintain your lifestyle.

It's never too early to start retirement income planning. The earlier you start, the more time you have to save and invest, and the more likely you are to achieve your retirement goals.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.