When dealing with partnership accounts, a sole proprietorship or partnership firm may be converted into a firm to derive advantages from improving efficiency and avoiding competition. Similarly, a sole trader or a firm can sell their business to a company (or convert it into a company) to derive the benefits of limited liability and increased capital. In other words, a joint stock company is formed to acquire the business of a sole trader or partnership firm. At present, by acquisition of a business, we mean the accounting entries involved in the purchase of a business of a non-corporate body by a corporate body. The business of a sole trader or a firm may be converted into a company or the business may be sold to an existing company. In both cases, the transaction becomes a business acquisition or business purchase. The company that acquires or purchases another business is called the purchaser or vendee (purchasing company) and the seller is called the vendor.

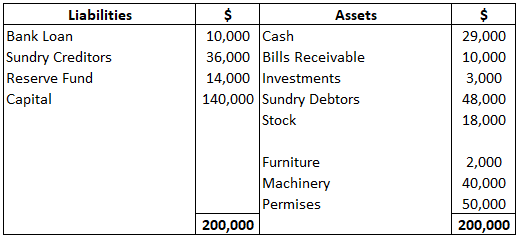

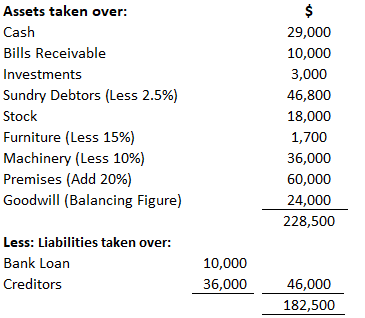

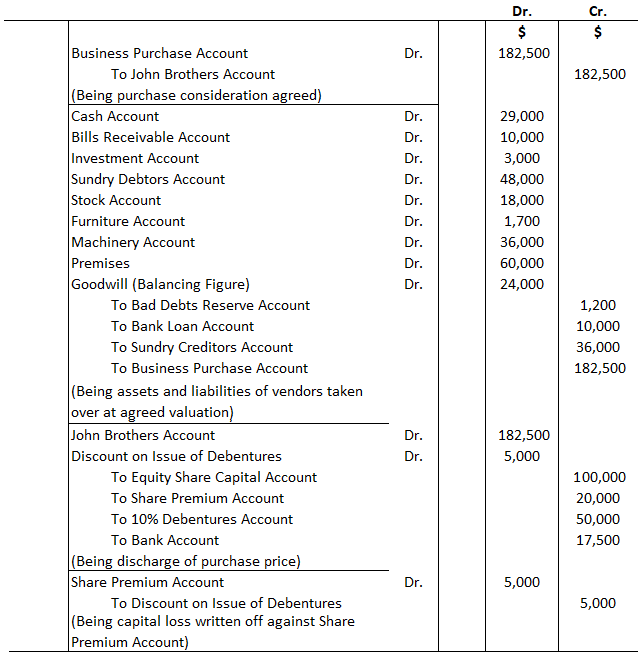

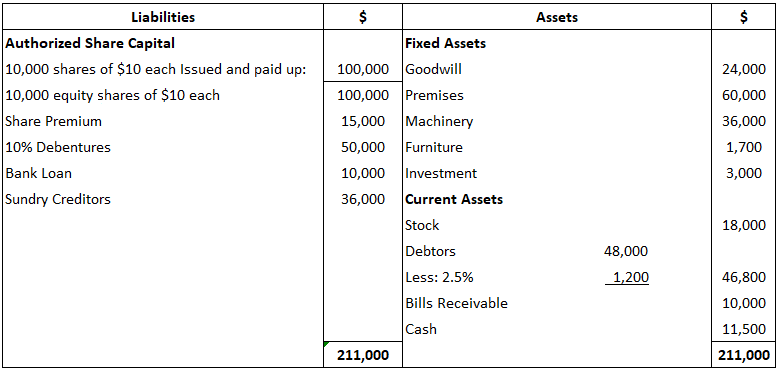

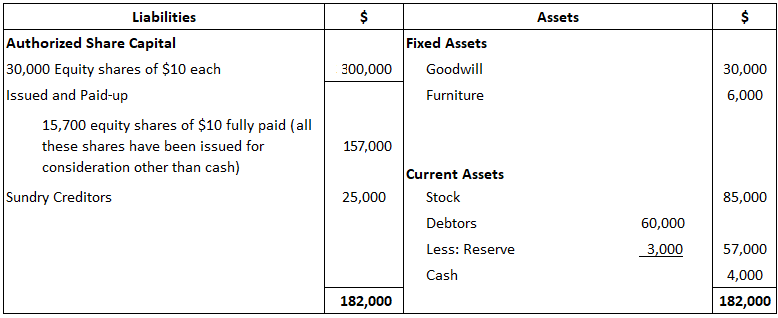

The vendor firm (i.e., the firm selling the business) and the vendee must agree on the price of acquiring the business. The purchase price, or purchase consideration, is the price payable by the purchasing company to the vendor as a consideration for the business taken over. This price is determined by an agreement between the vendor and vendee. The price can be paid by the purchasing company in cash, shares, or debentures. In certain cases, the purchase price is paid using a lump sum. In such cases, to determine whether the price paid is lower or higher than the value of the net tangible assets of the business, it is necessary to compare the lump sum with the net tangible assets taken over. There are two main methods for calculating purchase consideration: first, the net asset method; and second, the net payment method. Under this method, the purchase price to acquire a business is calculated by adding up the value of all assets taken over by the vendee less the amount of liabilities. For instance, X Ltd. is a firm whose tangible assets are valued at $200,000 and liabilities at $45,000. Then, for this company, the net assets or net tangible assets amounts to $155,000. Normally, the purchase price and the net assets are equal. However, in many cases, the two figures may be different. Using the net payment method, the purchase price is determined by adding up the various payments made by the purchasing company. For instance, a purchasing company discharges the purchase price by the issue of 1,000 shares of $100 each, 200 debentures of $100 each, and a cash payment of $30,000. In this case, the purchase price is $150,000 ($1,00,000 + $20,000 + $30,000). The purchase price must be compared with the net assets acquired. If the amount paid exceeds the net assets acquired, then the excess amount is to be debited to goodwill. In certain cases, the amount paid may be less than the net assets acquired. Therefore, the excess amount (i.e., the capital profit) is to be credited to the capital reserve. When the value of net assets is calculated, the revised values of assets and liabilities must be taken into account. If the revised values are not given in a problem, then you should use book values. When the business is handed over, liabilities along with assets (including cash at bank and cash in hand) are taken over by the purchasing company. Here, liabilities means external liabilities (the amount payable to third parties) and assets means non-fictitious assets. There may also be either a capital loss or a capital gain. If there is a gain, then there cannot be a loss; similarly, if there is a loss, then there cannot be a gain, out of the same transaction. In accounting, there are two ways to treat a business acquisition: (A) New set of books are opened; and (B) the same set of books are continued. The following are the entries recorded by the purchasing company: Note: If the purchase price exceeds the net assets, the excess amount is debited to the goodwill account. If the net assets exceed the purchase price, the excess amount is credited to the capital reserve. Note: Any difference between the debit and credit totals is debited to the goodwill account or credited to the capital reserve account. B.K. Limited, registered with a capital of $1,000,000 in equity shares of $10 each, acquired the business of John Brothers. The balance sheet of the firm at the date of acquisition was as shown below. The assets and liabilities were subject to the following revaluation: Required: Show journal entries in the books of the company and prepare the balance sheet. Calculation of Purchase Consideration Journal Entries in the Books of B.K. Limited Balance Sheet of B.K Limited as on ........ Sometimes, the purchasing company does not take over the book debts and trade liabilities belonging to the vendor. This is because the complete recovery of the amount against book debts may not be possible and trade liabilities may be more than the estimated figure. For this reason, taking over the vendor's debtors and creditors comes with an associated risk. In certain cases, the purchasing company takes over the book debts on a guarantee given by the vendor for their realization. An agreed amount is retained against the vendor guarantee account. The amount is adjusted against the purchase price. That is to say, the purchase price is paid after deducting the guarantee amount. If the full amount is realized, the guarantee amount is returned; if not, the guarantee account is debited to the extent of loss and the balance is paid. The purchasing company may charge a nominal commission for the job done on behalf of the vendor. As an alternative to the above, the purchasing company takes the responsibility of collecting from debtors and paying off creditors, serving as an agent for the vendor. For this service, the company charges a commission at an agreed rate. The entries to be passed by the purchasing company in such cases are as follows: Alternatively, when no record is maintained in the books of the purchasing company, only the receipts and payments and payments on behalf of the vendor are recorded in the vendor's current account. The journal entries are: A limited company acquired the business of Mr. David with the exception of his trade debts and trade liabilities. The company, however, agreed to collect his debts amounting to $100,000 and pay off his creditors amounting to $45,000. All the sums due from his debtors were collected except $3,000 in bad debts and $2,000 allowed as cash discount. The creditors were paid $43,000 in full settlement. The company agreed to do this job against a commission of 2% on the amounts collected and 1% on payments made. Required: Show the ledger accounts for the company, assuming that the amount due to the vendor was paid off. Ignore interest. Solution Alternatively: When a business is converted into a company, it is sometimes the case that no new set of books is opened; instead, the purchasing company decides to continue with the same set of books. In such cases, the books of the old business are converted into the books of the new company by passing certain adjustments and transfer entries. There will be no closing entries in the books of the old firm nor opening entries in the books of the company. However, the following points may be kept in mind. A and B are in partnership, sharing profits and losses at the ratio of 3 : 2. They wish to dissolve the firm and sell the business to a limited company on 31 December. At this point, the firm's balance sheet appears as follows: A limited company with an authorized capital of $300,000 in equity shares of $10 each is registered to purchase the above business on the following terms: The auto assets are not required by the company, and A takes over it at an agreed valuation of $8,000. The purchase consideration is satisfied by the issue of equity shares of $10 each at par. Required: Show the journal entries and balance sheet for the company, assuming that the same set of books is continued. Balance Sheet as on 31 DecemberWhat Does the Acquisition of a Business Mean?

Purchase Consideration

Calculation of Purchase Consideration

Methods to Calculate the Purchase Consideration

A. Net Asset Method

B. Net Payment Method

Goodwill or Capital Reserve

Accounting Treatment for the Acquisition of a Business

A. New Set of Books Are Opened

Example

Solution

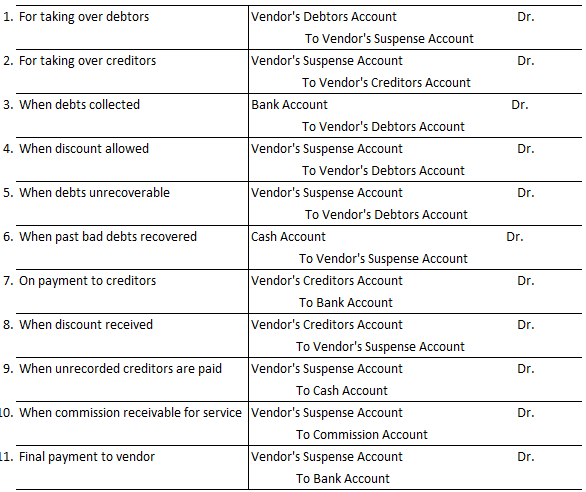

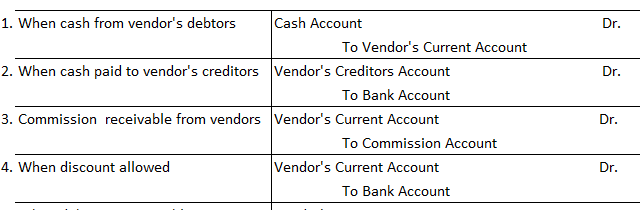

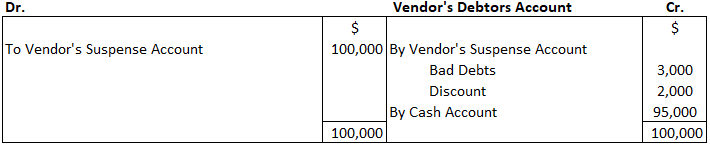

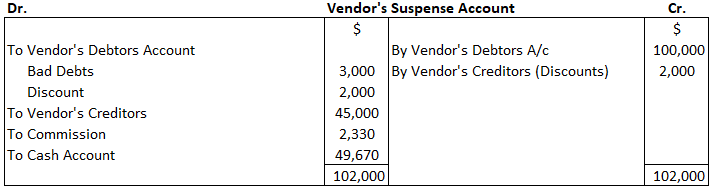

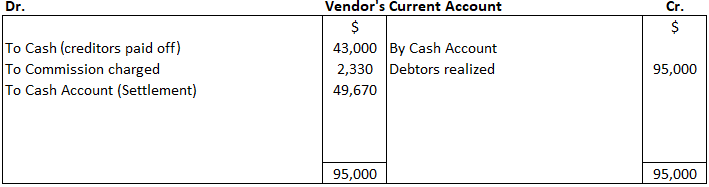

Vendor's Debtors and Creditors

Example

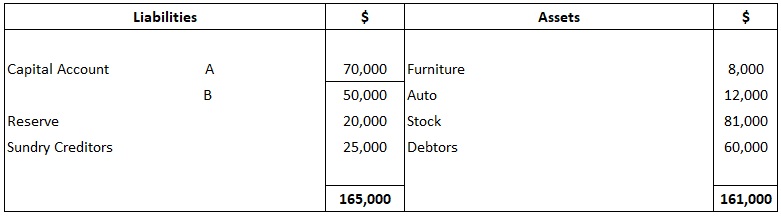

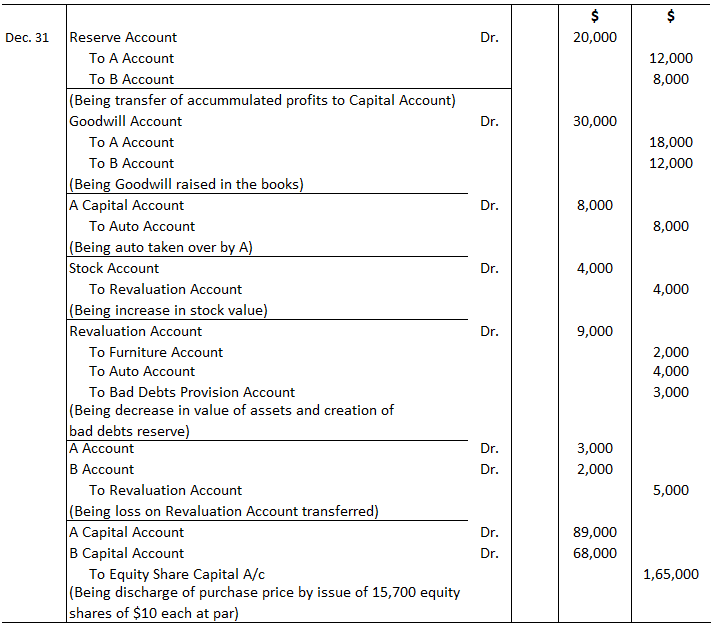

B. Acquisition of Business by Continuing the Same Set of Books

The revaluation account, as in "Admission of a Partner," is closed by transferring to capital accounts.Example

Solution

Acquisition of a Business FAQs

The acquisition of a business typically involves conducting research and due diligence on the target company, negotiating terms of the deal with the seller, and completing any necessary financing or legal steps.

Suitable businesses to acquire can be identified through a variety of sources, including industry contacts, advisors and brokers, online marketplaces and databases, or even attending industry events.

Before making an offer for a business, it is important to conduct thorough research and due diligence on the target company. This includes examining financial documents as well as engaging legal advisors to assess potential risks.

When negotiating an acquisition, factors such as the purchase price, terms of payment, and warranties should all be taken into consideration. Additionally, the seller and buyer should agree on how to handle any potential liabilities or disputes that may arise after the transaction has been completed.

Yes, depending on the structure of the transaction and other factors, it is possible to structure an acquisition as a tax-free transaction. It is recommended that both parties engage legal and financial advisors to ensure the process adheres to all applicable laws and regulations.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.